Anit Hoarding - sgml/signature GitHub Wiki

Zakat as an Instrument for the Prevention of Hoarding Suad N. Bećirović International University of Novi Pazar St. Dimitrija Tucovića bb Novi Pazar, Republic of Serbia E-mail: [email protected] ABSTRACT There is a consensus among economists that money has three basic functions: medium of exchange, unit of account and store of value. However, it is often ignored that the functions as medium of exchange and store of value are contradictory, because when economic subjects save money, it loses its function as medium of exchange, which can lead to deflation. In order to develop an efficient financial system, instruments to attract savings have to be developed. Theorists of the capitalistic economic system insist on the interest rate as the best way for savings mobilisation. The interest rate is not a viable alternative for the Islamic financial system due to the fact that interest is forbidden Islam. Furthermore, the problem of money hoarding and the occurrence of interest are interrelated. Hoarding leads to the formation of interest and therefore without an efficient prevention of money hoarding, the goal of developing an interest-free economy cannot be achieved. For the development of instruments for the prevention of hoarding, first the characteristics of money and the behaviour of savers have to be studied in detail. Especially, money has to be understood from the Islamic perspective, which includes the analysis of the rules of money exchange with regard to the prohibition of interest (riba). Moreover, traditional methods for the prevention of hoarding in the capitalistic and other economic systems have to be analysed. After conducting the research mentioned above, we concluded that zakat is a viable fiscal instrument to solve the problem of hoarding of money, because it is paid on a wide range of different assets, and a motivator to increase the supply of money, as those individuals who do not use their savings for investments will lose 2.5% percent of their savings annually. Thus, zakat is not only a religious obligation, but also an important economic instrument. Key Words: saving, hoarding, interest, zakat.

- INTRODUCTION Money is an indispensable part of our life. Any economic activity, even simple transactions, cannot be executed efficiently without money. If we would assume an economy without a standard medium of exchange, then we would have had a barter economy. In a barter economy, every participant in the economy changes the goods he possesses. Such a situation is described by famous Islamic scholar Abu Hamid Al-Ghazali in the following way: "Sometimes a person needs what he does not own and he owns what he does not need. For example, a person has saffron but needs a camel for transportation and one who owns a camel does not presently need that camel but he wants saffron. Thus, there is the necessity for a transaction in exchange. However, there must be a measure of the two objects in exchange, for the camel-owner cannot give the whole camel for a quantity of saffron. There is no similarity between saffron and camel so that equal amount of that weight and form can be given. (…) These goods have no direct proportionality so one cannot know how much saffron will equal a camel’s worth. Such barter transactions would be very difficult." (Ghazanfar & Islahi, 1997, p. 27) Here, Al-Ghazali describes the disadvantages of barter. The first problem with barter is that it is difficult to specify the value of a merchandise, because there is no standard medium of exchange. It is difficult to specify, for example, how much saffron is necessary to buy a camel, 2 especially when the object of exchange is a unique object, e.g. a camel, because every camel is different. So, we have to be able to assess the value of different goods. The more goods exist in an economy, the more relative values would be needed. For example, if ten commodities are traded, we would need 45 prices 1 ; if 100 goods are traded even 4,950. (Mishkin, 2004, p. 46) Therefore, it is necessary to introduce a standard measure for value, in order to exactly know the price of a certain product measured in a standard unit. By using a standard measure we have one price for one good. This introduction facilitates trade in the economy and increases transparency. The second problem is the need for products. In a barter economy goods are exchanged, and anybody who wants to procure a needed product must possess an attractive product to offer on the market. In fact, every person in the barter economy has to be a trader and has to own marketable goods. In such a scenario, it can take a long time and effort to find a suitable partner for the barter transaction. Moreover, it is possible that the buyer of an exchanged good is not a specialist at the trade of certain goods. For example, if the camel owner accepts saffron, maybe he does not know where the markets of saffron are, thus he has to invest time and money in order to find customers for saffron. This lost time hinders the buyer from his main business, e.g. the trade with camels. So, the use of barter would cause lots of transaction costs to every party. To solve this problem, a general accepted medium of exchange is needed, which will be accepted by everybody. Furthermore, if the camel owner accepts a big quantity of saffron, the question arises what to do with such a big quantity. First, he must be able to store such a great quantity; second, if he wants to buy other goods with this saffron, it is not sure whether another participant in the economy will accept this merchandise from him. This long waiting period until the sale of the goods is very problematic for perishable goods (e.g. milk, eggs). But, if the owner of the saffron is unable to find a customer until the goods are ready for sale, he will lose his "purchasing power". Therefore, money should store purchasing power over time and not lose its value immediately. Money holders want to have a longer "time-to-market", without pressure to consume their money immediately. Another problem at a barter exchange occurs when one party has only a small quantity of merchandise to change, e.g. saffron, but the other party has only a camel to offer. So the question arises how to carry out such a transaction, because a live animal cannot be divided into several parts. Therefore the medium of exchange has to able to be divided into small parts, in order to be able to show the value of less valuable goods and thus enable such an exchange. From the above discussion, we can see the major functions money has in the economy:

- Medium of Exchange and Unit of Account. Money enables the acquisition of every kind of goods and services in the economy. As standardised medium of exchange, money minimises the time and costs at exchanging goods and services. The existence of a general accepted medium of exchange also leads to the standardisation of the measure of value in the economy. Due to these benefits, the question arises what kind of material should be used as medium of exchange. Any material used for money has to be scarce and divisible. In order to be accepted by every economic agent the material used as money should be very difficult to reproduce, in order to keep the supply relatively low. And, as already said, the medium of exchange should be able to be divided into small parts, so this it is able to show the value of less valuable goods and thus enable such an exchange.

- Store of Value. Money represents the right for a holder to buy certain products offered in the economy. Money holders usually want to preserve this flexibility, because they do not want to have the pressure to consume money immediately. Therefore, a material has to be chosen, which is durable over time, or can be substituted without an increase in supply. But, the majority of materials available can only be used a limited period of time. For example, some food can be used only for a relatively short period (e.g. dairy products), salt loses its value when mixed with water or the majority of metals rust and lose their value. As a general medium of exchange different materials, which had a certain value for the participants in the economy, such as animals, weapons, salt, grain etc. have been used, but especially precious metals were popular as medium of exchange have been used during history. (Davies, 2002) When we analyse the criteria for choosing a material to become money, it is 1 This can be calculated with the formula: ( ) 3 understandable why gold and silver were used most frequently as medium of exchange. Their availability is very limited, especially of gold, so these precious metals represent purchasing power, i.e. these metals are accepted by everyone. Furthermore, these precious metals can be divided easily into many small parts. So minting coins is relatively easy. And the most important condition, durability, is only fulfilled by precious metals. Gold and silver do not spoil, do not become out of date, do not rust and do not break. Moreover, gold and silver can be stored easily, because they do not lots of space. Contrary to gold and silver, most other materials do not fulfil the three conditions mentioned above and therefore are not efficient for using as medium of exchange.

- THE CAUSE FOR HOARDING AND ITS CONSEQUENCES The introduction of money in an economy facilitates the development of the economy. All offered goods and services in the economy can be sold and bought with money. Therefore, as Gesell points out, "money describes a circle, which it eternally passes through; it reverts back to the starting point." (p. 104) While the goods and services in this process will always be different, the used money will always be the same, because money enables a person to buy all goods and services offered in the economy at a certain price and pay without any problems. This flexibility is not offered by any other good, not even with other securities, e.g. cheques or bills of exchange. This "superiority" of money was also highlighted by al-Ghazali when he said: "When one owns money, one owns about everything, not like the one who owns cloth, as he owns cloth and nothing else." (Islahi, 2001, p. 3) The flexibility of choice, which is the essential function of money as medium of exchange, is the reason why sometimes the value of commodity money (e.g. produced of silver) was higher than the price of the raw material of the same weight. Therefore we can say that money is not a "veil" for all goods and services offered in the economy - it enables choice for its holder and therefore a big advantage compared to other economic agents. It is the general accepted medium of exchange and this function can be described as the public function of money. When we analyse the continuous circle of selling and paying for goods and services, we can see that there is a major difference in the behaviour of sellers and buyers (money holders) with regard to flexibility of exchange. On the one hand, every seller has to sell his products continuously on the market in order to earn an income. If the seller is unable to sell his products, he will reduce the prices to promote the sale of his products. German-Argentine economist Gesell explains this situation in the following way: "One can say (...) that the supply (of products) is subject to a powerful, everyday growing, all obstacles overcoming, in the material containing compulsion, a compulsion which is appended naturally to the things offered. The offer cannot be delayed. Regardless of the owners’ will, the goods have to be offered on the market every day." (p. 140) So providers of products have the pressure to offer their products every day, unless their products will lose their value. On the other hand, this is not true for the money holders. Money holders use their for money for transactions (consumption and investments), but also part of the income will be used for savings. The reason for saving can be for future consumption (e.g. marriage, retirement, buying expensive products), protection against future unexpected expenses, or simply having temporarily higher receipts than expenses. But money holders can keep this saving in the form of money and do not have the pressure to consume it immediately. This is also described by Gesell in the following way: "The demand (for products) is, on the other hand, as I said before, free of such coercion. Produced of gold, of a precious metal, which, as its name implies, has an extraordinary position among earthly substances and, so to speak, can be seen as a foreign substance of this earth, (because) it resists victoriously all forces of nature. Gold does not rust and not fault, it does not break and does not die. Frost, heat, sun, rain, fire – nothing can hurt it. The money, we make from gold, protects its owner against any material loss." (p. 140) Here Gesell, describes the resistance of gold money against every natural enemy. The same is also true for fiat money, because we can change any banknote at the central bank if a note is damaged. So, we can conclude that besides the flexibility of choice, there is another major difference between money and other assets. Most assets, except money, suffer some wastage or involve some storage cost through the mere passage of time, irrespectively whether they were used to produce a yield or not. 4 However, the hoarding of money does not cause such storage costs and therefore money holders can always withdraw their money from the markets without real expenses. Due to this possibility, money performs the function as a store of value, i.e. everybody can receive money and store it, because he can transform public legal tender into private ownership - this can be called the private function of money. However, when economic subjects hoard money, it loses its public function, because other economic agents cannot use this hoarded money anymore. We can see that money has two contradictory functions. By hoarding money, it becomes a purpose of its own. Abu Hamid al-Ghazali described the hoarding of money in the following way: "Anyone who uses money contrary to its objectives or functions is ungrateful to the bounty of Allah. If someone hoards dirhams and dinars, he is a transgressor. He would be like a person who imprisons a ruler, thus depriving the society of the benefits of his benevolence. Dirhams and dinars are not created for any particular persons; they are useless by themselves; they are just like stones. They are created to circulate from hand to hand, to govern and to facilitate transactions. They are symbols to know the value and grades of goods." (Ghazanfar, Islahi, 1997, p. 29) Here, Al-Ghazali emphasises that money should only be used as medium of exchange. Indirectly, al- Ghazali said that money should not have any material value to avoid the hoarding of money by saying: "they are just like stones". This position was also held by other Islamic scholars. For example, Ibn Taymiyah said: "Athman 2 has to be the measure for objects of value, through which the quantity of the objects of value are recognised, and they are never intended for consumption." (Islahi, 1996, p. 262, 263) And Ibn Taymiyah's famous student Ibn al-Qayyim said: "Cash and coins have no purpose of its own, they are intended to be used for the acquisition of goods." (Islahi, 1996, p. 263) So the question arises, why did Islamic scholars emphasise to use money only as medium of exchange, but not to hoard it (to use it as store of value)? The answer can be found again at al- Ghazali, when he connects hoarding and taking interest by saying: "One who practices interest on dirhams and dinars is denying the bounty of Allah and is a transgressor, for these coins are created for other purposes and are not needed for themselves. When someone is trading in dirhams and dinars themselves, he is making them as his goal, which is contrary to their objectives. Money is not created to earn money, and doing, so is a transgression (…) The two kinds of money are means to acquire other things; they are not meant for themselves. In relation to other goods, dirhams and dinars are like prepositions in a sentence; as the grammarians define them, ‘a preposition is that which is used to give proper meaning to words,’ or their position is like a mirror reflecting colours (of other things but no colour of its own). If a person is permitted to sell (or exchange) money with money, then such transactions will become his goal, and as a result will be imprisoned and hoarded like anything. Imprisonment of the ruler or a postman is a transgression, for they are then prevented from performing their functions; same is the case with money. It is a transgression." (Ghazanfar & Islahi, 1997, p. 31) Here, we can see that al-Ghazali describes hoarding as the "imprisonment" of money, by which the hoarder inflicts injustice to all other economic agents, by asking for an unjustified income. The hoarding of money leads to the monopolisation of the general accepted means of exchange. So, demanders for money are deprived of the general accepted medium of exchange and have to pay a price (interest rate) in order to receive it. Thus, hoarding of money leads to the formation of interest. The possibility to hoard money without storage costs enables money holders to control the supply of money, because they can store their savings without any losses. Money holders do not have to fear losses due to perishing and they do not have to fear they will lose customers, because they own the general accepted medium of exchange. So, if they hoard (store) money and want to lend it for a specified interest rate, they will find enough customers who are willing to pay the interest. And if a money holder thinks that the current interest rate is too low, he can hoard his money, i.e. change his investment portfolio. If the demanders are not ready to pay a higher interest rate, money lenders can wait, but the demanders for money cannot wait, because they need the money - companies for investments, households for consumption, the state for its public duties -. To receive the needed money, the demanders have to improve their offer. 2 Sing. thaman, the price or what is to be paid as the price, money, etc. 5 Figure 1: Development of interest rates for savings deposits with an agreed maturity of 12 months in Germany Source: Deutsche Bundesbank It could be assumed that the long-term accumulation of money savings will lead to a reduction in interest rates, which would be positive for economic development. However, a look at the development of interest rates shows that interest rates never fall to 0%, contrary to other prices. For example, figure 1 shows the development of interest rates for savings deposits with an agreed maturity of 12 months in Germany for the period from 1967 to 2003. The reason for not including newer data is that since 2004 Deutsche Bundesbank uses the methodology of the European Central bank, so numbers cannot be compared adequately. But, it can be seen that interest rates are always above 1 percent, despite a continuous decline since 2000. This shows that interest rates have to be positive in order to attract savings. As a result, the only reason for receiving an income from interest is that the unfortunate situation of another contracting party is exploited. Islam has forbidden the exchange of goods of the same genus with an excess, so a good does not lose its main purpose. In such a context, we have to understand the words of Ibn al-Qayyim about the prohibition of riba al-fadl and riba an- nasi’ah: "The secret which is behind the prohibition of unequal exchange of the same kind of precious metals is the preservation of their basic purpose, i.e. liquidity; and the reason for the prohibition of unequal exchange of the same kind of food is the preservation of their basic purpose, i.e. using as food." (Islahi, 1996, p. 263) Money is to be used for exchange, foodstuffs are meant for nutrition. Money and foodstuffs are needed by every economic agent. Hoarding of both will lead to an exploitation of demanders. Therefore Islam stipulates detail rules in which way goods with monopoly power can be used in order to develop just contracts between contracting parties. So, if someone wants to invest money, he has to share the risk with the demander or give him an interest-free loan. Another possibility is the exchange of a physical asset for money with a delay. In such a case a physical asset, which has no monopoly status is exchanged and therefore an individual cannot monopolise a merchandise. The hoarding or monopolisation of money or any other goods would not happen, if these goods had not have special characteristics, which cause a high demand for them.

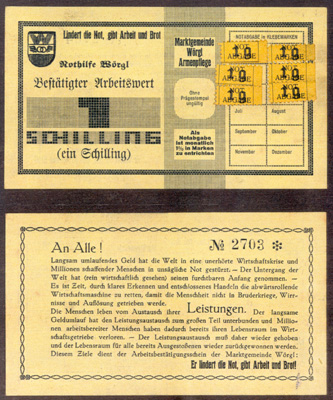

- HOW TO RETURN HOARDED MONEY TO THE ECONOMY? The previous section has shown that money has two contradictory functions - a pubic and a private function. The question arises how to return the hoarded money to the economic circle, so it can perform its major function as medium of exchange. While developing an adequate concept, money should not lose its quality as medium of exchange, but hoarding should be hindered. Economists have always developed concepts to attract savings to the financial markets. 6 Capitalistic economists insist that the interest rate is the best mechanism to attract savings. However, as we have mentioned before, only a positive interest rate can attract savings. If this interest is perceived to be too low, money will be hoarded again. In order to keep the interest rates at an attractive level English economist John Maynard Keynes proposed that the government should create an additional demand for goods and services in order to increase demand for money. Keynes said that "even a diversion of the desire to hold wealth towards assets, which will in fact yield no economic fruits whatever, will increase economic well-being. In so far as millionaires find their satisfaction in building mighty mansions to contain their bodies when alive and pyramids to shelter them after death, or, repenting of their sins, erect cathedrals and endow monasteries or foreign missions, the day when abundance of capital will interfere with abundance of output may be postponed. ‘To dig holes in the ground’, paid for out of savings, will increase, not only employment, but the real national dividend of useful goods and services." (p. 139) Keynes suggests that any investment which is able to mobilise savings (avoid hoarding) is good in order to boost the economy and decrease unemployment. With regard to Islamic finance it is quite clear that interest as a concept to attract savings is irrelevant due to the prohibition of interest (riba). Interest is also not an important concept to attract savings from an economic perspective, because such a system can only work with positive interest rates. But, someone could say that government intervention, such as public investments, would be necessary to increase the profitability of Islamic bank accounts and so the motivation to invest money on the Islamic financial markets. However, what Keynes did not consider is that these government interventions are not one-time interventions, but interventions, which are of a dynamic nature, which have to be conducted regularly in a certain time frame. Therefore, the long-term consequence of government interventions are rising public debts, because in times of economic crises public revenue decreases due to a decline in economic activity, whereas expenditures rise due to higher social expenses and government interventions (e.g. subsidies). When the economy recovers, revenues rise again and should be used for repayment, but the problem is that expenditure do not fall simultaneously with economic recovery, because granted subsidies or long- term investment projects cannot be cancelled easily. Therefore, in our opinion, this concept is not sustainable on the long-term and not an interesting one to attract savings. Instruments for avoiding the hoarding money should not reward the hoarders, such as it is the case in an interest-based system. Hoarders should pay a kind of storage costs on their money. By paying such costs, the question also arises who will receive this income. Therefore, in the following sections, we will analyse some alternatives for the prevention of the hoarding of money with regard to these criteria. 3.1. Inflation as an instrument to avoid hoarding of money Another instrument proposed by Keynes to attract hoarded money is inflation. With inflation, Keynes wanted to introduce "carrying costs", so the hoarding of money will become expensive. An increase of the money supply by the central bank should motivate money holders to avoid the hoarding money and instead consume or invest their liquidity. The first problem with this concept is that in this case the central bank will offer more money to the commercial banks. However, it is not sure that the banks (or their clients) will accept this additional offer. The willingness of economic agents to demand the money depends on their expectations. If they are pessimistic, the additional money will not be demanded or go into the so- called "liquidity trap". This "liquidity trap" makes an efficient monetary policy very difficult. (Keynes, 2003, p. 112) Thus, monetary policy will not be adequate to solve an economic crisis and even create more liquidity problems in the economy, which can lead to a deflation. The best modern example for this is Japan. In January 2016, the bank of Japan announced it had cut the rate on excess cash reserves to minus 0.1% in its latest attempt to reinflate the country’s economy, i.e. institutions will have to pay the central bank for the privilege of parking reserves that exceed those required by regulators. (Watts) Similar moves have been also employed by the European Central Bank and the central banks of Switzerland, Sweden and Denmark. In order to avoid that additional cash goes to the "liquidity trap" a reliable demanders for money will be sought. This "chosen demander" will be the state, whose bonds will be bought by 7 the central bank. The consequence of such action will be higher public debts and an increase of the inflation rate. So, the problem with this proposal for hoarding prevention is that an intermediary is needed to cause a higher inflation rate. But the question is, who will pay the price of this action? Inflation could be, at first sight, a solution for the hoarding of money, especially in a closed economy. A high rate of inflation decreases the motivation of money holders to hold cash and to invest the money in the financial markets. Another positive aspect of a short-term rise of the inflation rate is that companies will have inflation gains on the condition that their costs will remain constant. These inflation gains will increase the marginal efficiency of capital and therefore increase investments. Keynes expected that costs, especially wages, will remain relatively constant over time, or lag behind in the adaptation of inflation, because he assumed money illusion. (Senf, 2007, p. 215) However, it is too simplistic to assume that other economic agents will not ask for changes of their prices. Suppliers will ask for higher prices, trade unions will also ask for higher wages and salaries. So, costs will adapt to the expected rate of inflation and eat up inflations gains. Without inflation gains, a new increase in money supply would be necessary in order to increase the marginal efficiency of capital to prevent an outflow of money into the liquidity trap. In extreme, this can lead to a high inflation rate. A higher rate of inflation will lead to several negative consequences. One of the major problems with inflation are income redistributions. All economic subjects, whose contractual rights are not adapted immediately to the rate of inflation, pay the price for inflation. Even indexation cannot solve this problem completely. It becomes a game of chance which contractual side will be the winner of a certain rate of inflation. Another loser of inflation are the taxpayers. Nominal amounts are subject to taxation and many countries have a progressive tax system, which will lead to the payment of higher taxes due to inflation. Inflation also leads to wrong resource allocations, because the prices of different kinds of products adapt at a different pace. For example, the prices of shoes adapt every month, whereas the prices of foods will adapt continuously. So the relative value of these goods changes. But this distortion is only caused by inflation and not due to efficiency gains. In extreme, economic agents can lose belief into the domestic legal tender and use foreign currency for exchange transactions. In such a case the financial system would not work efficiently, because savers would hoard their savings in foreign currencies and physical assets which are more resistant to inflation. So economic agents would have severe problems in receiving funds for their investments and consumption. Therefore, we can conclude that there are more losers of such a system than winners. Cash holders are taxed by this system, but they can change their investment portfolio or use foreign currency to preserve their savings. Those money holders who lend their money on interest, will adapt the nominal interest rate according to the inflation rate, which can lead to an extreme rise of interest costs for debtors. In such a system, money holders will not be penalised for hoarding, but the price has to be paid by economic agents who can adapt their prices flexibly, especially the working class and smaller companies. 3.2. A tax as an instrument to attract savings German-Argentinean economist Silvio Gesell had a quite different idea how to attract savings. Gesell’s goal was to develop a kind of money which can only be used as medium of exchange, but not as store of value. In order to eliminate the hoarding of money, storing money should become as expensive as the hoarding of goods. Only if hoarding causes storage costs, money holders would be in the same position such as owners of physical assets, i.e. there would be no superiority of money anymore. Gesell proposed a tax on hoarded money, so money holders should be motivated either to consume or invest their money (either directly or give their savings to the bank even without an interest income). In detail, this proposal looked like this: The so-called "free money" loses one-thousandth (0.1%) of its nominal value every week, which has to be borne by the money holders. Every banknote has extra space, where the owners have to stick small change (which looks similar to stamps 3 ) on the note, in order to keep its nominal value. Because banknotes lose their value every week, owners will certainly want to 3 Therefore Irving Fisher called this type of money "Stamp Scrip". 8 forward their money as quickly as possible. (Gesell, 1949, p. 183) However, if he keeps (hoards) his banknotes, e.g. for four weeks, his banknotes will lose 0.4% of its nominal value and 5.2% annually. In fact, the concept of linear depreciation of assets is now applied to money. With this linear decrease of the nominal value of money a continuous circulation of money is made possible, which will cause that everybody will pay in cash, pay back his debt and bring the remaining cash surplus to the bank, which has to look immediately for customers in order to avoid storage costs. Therefore, banks will offer money at lower interest rates. At the end of the year, all existing banknotes will be exchanged against new ones, in order to have space for new stamps. By introducing hoarding costs, the hoarding of money will be avoided. This will have two consequences: first, a continuous flow of money will be guaranteed; second, money holders cannot misuse their monopoly position and ask for interest. In this way, the supply of money would rise, which would again lead to a fall of interest rates at about zero percent, according to the law of supply and demand. Moreover, the velocity of money would increase. Inflation will not be caused by this increase in money supply, on the condition that money supply is regulated according to the changes of the gross domestic product. (Senf, 2005, p. 124) The ideas of Gesell have been implemented in the Austrian municipality of Wörgl in 1932/33. At that time, deflation, originated by a reduction in the quantity of money by the Austrian central bank, caused mass unemployment. In order to tackle this economic crisis, the municipality Wörgl began to pay its employees with "free money". Also, a number of local companies participated in this experiment. This led to the acceptance of free money by the local population. A distinctive feature of free money was that each banknote contained twelve fields – for each month. By the end of the month, in order to preserve the nominal value of the banknote, a label had to be bought for 1% of the nominal value of the banknotes. So, if someone had hoarded his banknotes for one year, he would have to pay 12 labels for 12% of the nominal value. In order to avoid this tax, people would spend their money as soon as possible or to leave their money in the bank. In this way, hoarding of money was prevented. Figure 2: "Free Money" used in Wörgl. On the right, stamps had to be stuck in order to keep the nominal value of the banknote Source: http://userpage.fu-berlin.de/~roehrigw/bilder/woergl1.jpg The hoarding tax caused an increased aggregate demand in Wörgl. The result of this experiment was the reduction of unemployment in Wörgl by 25 %, while unemployment increased in other parts of Austria. The local economy recovered from its crisis and municipal budget revenues increased. (Senf, 2005, p. 123) However, the further use of free money was prevented by the Austrian Central Bank, with reference to its monopoly of issuing money. The major disadvantage of Gesell’s theory is that he does not go one step further to describe investment opportunities of a saver in detail. By introducing the hoarding tax, the hoarding of "free money" would not be attractive anymore. Therefore, savers would look for other investment opportunities. Here, the saver has the following alternatives: foreign exchange securities physical assets A saver can change "free money" into a stable foreign currency (for example dollar, euro). He would only use "free money" in exchange transactions, while using foreign currency for hoarding, on which the hoarding tax has not to be paid. A similar process can be observed in the 9 countries with high inflation, where residents use local currency only for the exchange of goods, while for hoarding a stable foreign currency is used. This problem could only be solved by regulating the exchange in foreign currencies through the central bank, which would only allow foreign exchange for companies or in special cases for private individuals. Another investment alternative are securities. If the investor buys securities on the primary market, the buyer enables a company to finance its projects. In this case the saver will not have any "free money" anymore and the company will invest the received money in fixed and current assets. Such an exchange of "free money" to securities is beneficial for the economic development. On the other hand, if securities are only traded on the secondary market, securities are bought and sold and in this way the investor is able to avoid the hoarding tax. The same applies, if savers invest in physical assets, especially real estate. However, we could argue that at the end of the process, after every transaction the seller receives money which he has to invest or consume again. That is undoubtedly right. But the problem is that more and more money would be spent on securities in the secondary market and real estate, which will lead to a sharp increase of prices in these markets. So, many savings would be used for speculative purposes, instead of being used in the economic circle, e.g. for buying goods and services or investments. The negative aspect of speculation is that it does not increase the gross domestic product and leads to an inefficient allocation of resources. In order to be complete, Gesell’s theory has to take these investment opportunities into consideration and to consider broadening the taxation of money to different forms of assets. Another arising question is who will receive the lost value of the "free money"? When a constant level of gross domestic product is assumed, then the decrease of value of 5.2% annually will go to someone. Gesell proposed that free money should be administered by a currency authority, which should circulate "free money" via the Ministry of Finance. (Gesell, 1949, p. 189) So, in fact the loss of value will go to the state, because the state has always to monitor money supply via the currency authority according to the development of the nominal gross domestic product and the velocity of money. Of course, if there is a recession, the "profit" of the Ministry of Finance will decrease, whereas at an economic boom it will absolutely rise. So the Ministry of Finance could use these specific tax receipts for wealth redistribution or any other projects of public interest. However, it could be also used inefficiently, e.g. for an increasing unproductive public administration or a rise in wages for civil servants. 3.3. Zakat as an instrument for the prevention of hoarding of wealth Analysing our research up to now, we can conclude that no analysed instrument has convinced us to be sufficiently efficient for returning hoarded money to the financial system. On the one hand, a system is needed to directly tax the money holder. But, this tax should not lead to the loss of the function of money as a general accepted medium of exchange and individuals should not have a kind of pressure to spend their money as soon as possible. For example, at Gesell's proposal, money would lose its value every week. So, people would have the pressure to consume their earned money as soon as possible, which is contrary to the goal of money holders, who want a certain degree of flexibility with regard to consumption. It can be assumed that under such circumstances, economic agents would use a substitute currency. Another point is that people want to store their savings, because they want to transfer their purchasing power to the future. They will invest into a form of wealth (portfolio), which will be the most suitable according to their needs. Therefore, this tax has to cover different types of assets. Finally, as already emphasised in our previous analysis, we have also to consider how to use the proceeds from this tax and who will benefit from such a tax. An important tool, which is able to fulfil the conditions mentioned above can be found in the teachings of Islam through the commandment of a "wealth tax" called zakat. The concept of zakat as a tax to counter the practice of hoarding from an economic perspective has not sufficiently been considered among Muslim economists. One of the few economists was Mahmud Abu Saud, who said: "(...) what is that system that Islam prescribes to Muslims to enable them to develop their economy without touching interest, which is prohibited usury? To me, the answer is zakat." (p. 25) 10 In Shari'ah the word zakat refers to the determined share of wealth prescribed by Allah to be distributed among deserving categories. (Al-Qardawi, p. xxxix) Under wealth, the following kinds of assets are understood: gold, silver, currency and jewellery commercial assets, bonds, stocks and shares salaries, wages, and professional incomes rents from buildings, plants, and fixed capital livestock agricultural products mining and fishing products For every type of asset there is a determined zakat rate, which the possessor has to pay. It is necessary to mention that zakat has only to be paid if a zakatable item is possessed during the "hawl" (minimum time) and its "nisab" (minimum amount which determines the zakatability) is exceeded. Every kind of asset has its own nisab and every kind of asset (with the exception of agricultural products) has to be owned one lunar calendar year. If the value of the wealth falls below the nisab during a lunar year, the hawl begins to count from the beginning. Moreover, all assets which are determined for personal use and can be classified as "basic need" are not eligible for zakat. Basic needs are those without human beings cannot survive, such as food, shelter, clothing, and items needed for a job, such as books for study and tools for work. (Al-Qardawi, p.

{kind=link}

- Moreover, if the owner of a zakatable asset is burdened by debts, which reduce the asset's net worth to below nisab,zakat is not obligated. (Al-Qardawi, p. 68) From an economic perspective, the first four categories of wealth mentioned above are the most important for our analysis. Therefore, we will analyse the way of calculating zakat for these assets in detail. Zakat has to be paid on gold and silver, no matter whether they are used in the form of coins or bullion, or even as ornaments and decorative materials. (Al-Qardawi, p. 123) The same applies to paper money, because it is the general medium of exchange today. The rate of zakat for gold, silver and paper money is 2.5%. The nisab of silver is 595 grams and the nisab of gold 85 grams. (Al-Qardawi, p. 130) In order to determine the nisab of paper money, the nisab of gold has to be multiplied with the current gold price in the according currency. (Al-Qardawi, p. 131) These kind of assets have to be in the possession of the owner for one lunar year. Zakat has also to be paid by the creditor for his receivables. Islamic jurists distinguish between two kinds of debts. One is a debt whose creditors hope to receive it back, meaning debts on parties who are capable of payment. Zakat is obligated on this category of debts annually, as if they were property under control. (Al- Qardawi, p. 58) Second, doubtful or dead debts, which are debts on individuals who are incapable of repayment or are denied by debtors. These debts are unzakatable for all past years. But when the debts are received, they should be treated as a newly earned asset and zakat has to be paid only for one year, like on any other newly earned asset. (Al-Qardawi, p. 59) From the perspective of returning hoarded money to the financial system, we can see that zakat is an important motivator, because every money holder has to pay annually 2.5% of his savings as zakat. If these savings had been never invested, a saver would have lost half of its savings after about 27 years. In this context we can understand that the Prophet, peace be upon him, urged the guardians of orphans to invest the funds of orphans in order that they would not be consumed by zakat. (Qardawi, p. 125) So, zakat clearly stimulates to invest saved money, which will enable demanders for money to receive necessary funds for consumption and investment. Moreover, it is important to mention that Shari'ah takes into account the social aspect of taxation - zakat has only to be paid when someone has savings above the minimum of nisab, i.e. the value of 85 grams of gold. With regard to the tax rate of 2.5%, we can say that this is a moderate rate, which is a good motivator for the money holder to invest, but does not cause too much pressure on him. Due to this moderate tax rate, proceeds from zakat will be higher, because the majority of payers will not regard it as a heavy burden. Abu Saud recommended to introduce an additional tax, alongside zakat, on money according to the proposals of Gesell, which were practiced in Wörgl. (Abu Saud, 2002, p. 26) Furthermore, he said that anybody who will give his savings to banks, would be exempted from paying this money tax as long as money is in deposit. (Abu Saud, 2002, p. 28) However, we do not agree with Abu Saud's proposal, because it will still have the negative effects of Gesell's proposal. An 11 additional taxation of money, compared to other assets, will lead to the use of foreign exchange instead of the national currency for transaction purposes and people will certainly invest more money in substitutes such as gold and silver or other precious metals. This was also highlighted by Ibn al-Qayyim when he said: "Zakat is an expression of the utmost justice, because had it been obligated every month or every week, it would have heavily burdened the rich, but if it were made once in a lifetime, it would not have satisfied the needs of the indigent. The best way was to make it once every year." (Al-Qardawi, p. 72) We are of the opinion that the original Shari'ah rulings should be applied. In this case, money holders (no matter what kind of currency he owns) will have to pay zakat of 2.5%. Furthermore, if he saves one part in the form of precious metals, he will also have to pay 2.5% on this value. Here it is important to mention that assets with the same calculation of the nisab are treated as one type, so gold and currency are treated as one type of asset and if their total value is above the nisab, the owner has to pay zakat. Analysing further the investment opportunities of a Muslim investor he could use the money to make an interest-free loan to another person. This is, of course, a good deed in Islam, but exempting such loans from paying zakat could lead to the evasion of paying zakat. Therefore, in order to prevent such behaviour the creditor has to pay zakat on his receivables. Another investment alternative would be the investment of savings into real estate, e.g. a plot of land or a flat. It could be argued that on such kind of assets no zakat has to paid, as mentioned earlier. In order to clarify this situation, it is necessary to differ between buying something for trading purposes or for personal use. All commodities obtained for the purpose of trading are zakatable. Trade covers two elements – the action of buying or selling, and the intention of making profit. These two elements must always co-exist in trade. Therefore, when someone buys something with intention of using the asset (for personal and household use), this is not trade. Changing the intention from selling for profit to personal use of an item removes its zakatability. (Qardawi, p. 167) It can be concluded that when an asset is used as a storage of value for the purpose of hoarding, then it is also zakatable. Thus, investing savings in unproductive types of wealth (precious metals, foreign exchange, real estate) will eat up the value by 2.5% annually, if the value of savings is above nisab. Therefore, a Muslim investor has a great motivation to invest his savings into productive assets. If someone decides to invest in bonds, then the hopeful receivables are zakatable every year at a rate of 2.5%. This rule also applies for shares, which are held for trading purposes. In such a case shares are treated as commercial goods and the shareholder has to pay 2.5% of their market value, including dividends. (OIC Fiqh Academy, p. 58) With regard to the investment into shares in order to benefit from dividends or becoming a partner in a company, there are different opinions among Islamic jurists. If the company is a trading house, then zakat has to be paid on trade assets of the company. If the trading house has trade assets equal to nisab of money or more at the end of a zakat year, it must pay its due zakat at the rate of 2.5%. (Al-Qardawi, p. 161) The fixed assets of the company, such as buildings, furniture, equipment etc., are not zakatable, according to the unanimous agreement of Islamic jurists. (Al- Qardawi, p. 169) When zakat is due, the trader will sum up the amount of money, add to it the value of inventory and the amount of hopeful receivables. On this total it is necessary to deduct the debts of the company and zakat has to be paid on the net value. (Al-Qardawi, p. 168) The inventory has to be priced according to current prices on the due dates of zakat. (Al-Qardawi, p.

- On the other hand, when the company rents assets (e.g. real estate, cars) or is active in industrial production, in other words companies with dominant fixed assets in their balance sheet, the generated net income (profit) is zakatable at a rate of 10%, because fixed assets are exempted from paying zakat. (Al-Qardawi, p. 244/245) However, other Islamic jurists insist that zakat on the income should be paid at a rate of 2.5%. (OIC Fiqh Academy, p. 4) The necessity to pay zakat by entrepreneurs and shareholders shows the justice of Islam so every economic agent has to pay a certain amount of zakat, according to their possibilities. Furthermore, companies have a further motivation to generate a higher profit, in order to distribute a yield above the zakat rate to investors. From an macroeconomic view it is also important to analyse the portfolio of savers. If savers hold mainly unproductive assets, this is a sign of distrust in the national financial system and a 12 reason for the government and its agencies to react. But it is always important to avoid pressure for savers and force them to put their money into the financial system. They have always freedom of choice with regard to handle their savings, because Islam emphasises the protection of property. Another important question with regard to zakat is: how to collect this obligation from the zakat payers? Here, some ideas are presented to collect zakat in a modern Islamic economy:

- Bank accounts. The collection of zakat from bank accounts is very easy, because the bank statement contains how much money is on the account, so it is very easy to determine the zakat obligation.

- Cash. The collection of zakat on cash seems to cause major troubles. However, one alternative here is to install a "RFID" chip into banknotes. For example, Austrian-German technology company EDAQS has developed a new form of cash. Banknotes are equipped with a highly encrypted RFID chip. With the aid of appropriate terminals, the cash system by the name of "DICE" can always request an executive remote devaluation of the notes. (DICE) This system can be used in the following way with regard to zakat payment: When zakat is paid on banknotes, the value of the banknote will be kept, but if the zakat is not paid, the banknote will automatically lose 50% of its value as a penalty. However, it would be necessary to provide an easy identification mechanism for the value of banknotes for all economic agents, for example through a mobile phone application.

- Foreign exchange. The government could introduce a measure that the holding of foreign exchange is only allowed for companies for international trade or when a private person travels into a foreign country. Furthermore, it would be allowed to hold foreign exchange in cash, but on special accounts at the central bank in order to avoid hoarding. Therefore, the zakat on foreign exchange could be calculated easily.

- Real estate. The acquisition of real estate is registered at the official real estate register. According to this data, it can be analysed whether someone owns more real estate than he really needs. Furthermore, every property has to be exclusively registered on the name of the owner and not on another name, in order to avoid registering the property of one person on different persons, who are not eligible for zakat.

- Securities. Securities can be issued in the form of registered securities so the zakat payer can be tracked easily. Here it is important to determine whether securities are held for investment or trading reasons, because zakat calculation is different. At any case, the issuing company (as well as companies in the form of partnerships) has to deduct zakat before paying dividends to its investors. Finally, it has to be analysed who will receive the zakat receipts. It has to be emphasised that zakat receipts cannot be used for any purposes by the collecting body; the recipients are defined exactly in the Qur'an in the following ayat: Zakat is for the poor and the needy, and those employed to administer the (funds); for those whose hearts have been (recently) reconciled (to Truth); for those in bondage and in debt; in the cause of Allah and for the wayfarer: (thus is it) ordained by Allah, and Allah is full of knowledge and wisdom. (Qur’an, At-Tawba: 60) Here, the most important groups are the poor and the needy, meaning people who have some wealth, but this wealth is not sufficient to pay for their standard of living for the whole year or people who have neither wealth nor income at all. Islam asks from the believers to sustain solidarity with other individuals. This solidarity means that believers should help each other in solving their problems, which includes also financial problems. According to Islamic belief it is important that a person understands that he or she should not only pursue selfish goals, but also think about the needs of other fellow citizens. By paying zakat, not only that poor people will receive an income, but richer people will have a feeling for responsibility towards other people. Such a system will avoid unjust distribution and concentration of wealth, which is the long-term consequence of an interest-based economy. The presence of a great concentration of wealth side by side with severe poverty cannot be tolerated in an Islamic society. The motivation of zakat payers for payment is higher, because they know that their paid zakat will go to the defined eight categories. In order to ensure this willingness for payment, the use of zakat receipts has to be transparent, so zakat payers know that their money is used for the defined purposes. 13 On the other hand the legal penalty for zakat evasion is mentioned by the Prophet, peace be upon him: "He who pays it seeking the reward from Allah will be rewarded and he who refuses to pay it, we shall take it from him, along with half of his wealth, and by the authority given to us by our Lord. The clan of Muhammad are not allowed to take anything of its proceeds." (Reported by Ahmad, al Nasa'i and Abu Dawud) This means that law-enforcement agencies of the state will collect half of the wealth of the hoarder and collect zakat in addition to the penalty. CONCLUSION The goal of this paper was to analyse different methods for returning hoarded money into the economic cycle. Hoarding of money is a problem, because other economic agents cannot use this money anymore. Because money can be hoarded without major storage costs, if there is no efficient mechanism to prevent hoarding, interest will occur as a result of the hoarding. In order to enable an efficient money supply as a prerequisite for the economic growth, we have proposed zakat as a general wealth tax to accelerate the process of investing savings. Zakat has been treated in Islamic literature from different perspective, especially from a legal perspective and as a social tool for poverty eradication. In this paper we presented that zakat not only as a religious duty, but also as a macroeconomic tool for mobilisation funds and as a tool for wealth redistribution. Zakat will enable the circulation of money, because if people do not invest their savings, they will have to pay a tax – not too low, but also not too high – on their assets. The rules for paying zakat considers the portfolio of an investors, so a saver has to pay zakat on different assets. As a result, zakat has not the disadvantage that it would only consider money as subject to taxation. In order to have an efficient taxation and circulation of goods and money, every commodity has to be considered for taxation. Furthermore, zakat asks for direct participation in business, because by only giving an interest-free loan someone cannot escape the payment of zakat. The revenues from zakat will be used for specific purposes, especially for poor citizens. This rule shows that zakat has not only the goal to mobilise idle resources, but also to foster solidarity among Muslims and to redistribute a small part of the wealth of the rich to the poor. Therefore, zakat is a kind of opposite from interest. By hoarding money and thus monopolising the general medium of exchange, someone can demand an additional amount alongside the principal. So, interest is a kind of ransom to receive necessary money. This leads to pursuing selfish goals and the society will face negative consequences due to this behaviour. On the other hand, zakat is paid by the wealthy, in order to avoid selfishness and to care for others. Individuals must pay zakat on their wealth, but can invest this wealth in order to increase it. REFERENCES

- Abu Saud, M. (2002). Money, Interest and Qirad (reprint). IIUM Journal of Economics and Management, 10(1), 1-30.

- Al-Qaradawi, Y.. Fiqh al-Zakah, Volume 1. Jeddah, Saudi Arabia: Scientific Publishing Centre of the King Abdulaziz University. Retrieved from: http://monzer.kahf.com/books/english/fiqhalzakah_vol1.pdf.

- Bećirović, S. (2009). The Characteristics of Money and the Efficiency of Financial Markets. Paper presented at the conference "Economic Policy and Global Recession", Belgrade, Serbia: Faculty of Economics, 499-506.

- Bećirović, S., Plojović, Š. & Ujkanović, E. (2010) The Impact of Interest on the Economy. Paper presented at the conference International Scientific Conference "Financial crisis", Bratislava, Slovakia: Slovak Statistical and Demographical Society, 34-45

- Creutz, H. (1997). Das Geldsyndrom, 4th edition. Berlin, Germany: Ullstein Taschenbuch. 14

- Dalkusu, I. N. (1999). Grundlagen des zinslosen Wirtschaftens. St. Gallen, Switzerland: Dike Verlag AG.

- Davies, G. (2002). A History of Money – From Ancient Times to Present Day. Cardiff, UK: University of Wales Press.

- DICE (Dynamic Intelligent Currency Encryption – Cash Security System). Retrieved from http://www.edaqs.com/products/dice-cash-security-system/

- Gesell, S. (1949). Die natürliche Wirtschaftsordnung, 9th edition. Lauf bei Nürnberg, Germany: Rudolf Zitzmann Verlag. Retrieved from: http://userpage.fu- berlin.de/~roehrigw/gesell/nwo/nwo.pdf.

- Ghazanfar, S. M. & Islahi, A. A. (1997). Economic Thought of Al-Ghazali. Jeddah, Saudi Arabia: Scientific Publishing Centre of the King Abdulaziz University. Retrieved from: http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.119.1381&rep=rep1&type=pd f.

- Ibn Rassoul, A. (2001). Handbuch der Zakah und der islamischen Wirtschaftslehre. Cologne, Germany: Islamische Bibliothek.

- Islahi, A. A. (1996). Ekonomske ideje Ibn Al-Qayyima. In Sadeq, A.M. & Ghazali A. (Eds.), Pregled Islamske Ekonomske Misli (pp. 249-277) Sarajevo, Bosnia and Herzegovina: El Kalem.

- Keynes, J. M. (1936). The General Theory of Employment, Interest and Money. Project Gutenberg edition, retrieved from: http://cas.umkc.edu/economics/people/facultypages/kregel/courses/econ645/winter201 1/generaltheory.pdf.

- Mishkin, F. (2004). The Economics of Money, Banking and Financial Markets, 7th edition. Boston, London: Addison-Wesley.

- OIC Fiqh Academy. (2000). Resolutions and Recommendations of the Council of the Islamic Fiqh Academy 1985-2000. Jeddah, Saudi-Arabia: Islamic Research and Training Institute.

- Senf, B. (2005). Der Nebel um das Geld, 8th edition. Lütjenburg, Germany: Verlag für Sozialökonomie.

- Senf, B. (2007). Die blinden Flecken der Ökonomie – Wirtschaftstheorien in der Krise, 4th edition. Lütjenburg, Germany: Verlag für Sozialökonomie.

- Topoljak, S. (2007). Zekat i sadakatul-fitr. Novi Pazar, Serbia: El Kelimeh.

- Watts, W. (Jan 30, 2016)What you need to know about the bank of Japan and negative interest rates. Retrieved from http://www.marketwatch.com/story/what-you-need-to- know-about-the-bank-of-japan-and-negative-interest-rates-2016-01-29