ESPP - nolanhergert/notes GitHub Wiki

Employee Stock Purchase Plan

What are the real-world differences in tax outcomes of when I choose to sell my ESPP shares?

In an effort to answer this question properly, I'm going to make a very important simplification. The reasons that people tend to give for holding ESPP shares for longer (get dividends, your incentives are more aligned with the company's, etc) also hold true when you hold INTC outside of your ESPP account. You can do Quicksale (sell immediately) and relatively immediately buy INTC with the proceeds in a taxable brokerage account and get the same treatment as above. That's what the attached spreadsheet assumes, because it eliminates the asset diversification discussion entirely (whether you want to hold INTC in your assets, a good topic to bring up in another question) and results in no difference in the asset value (the final price is the same in all scenarios).

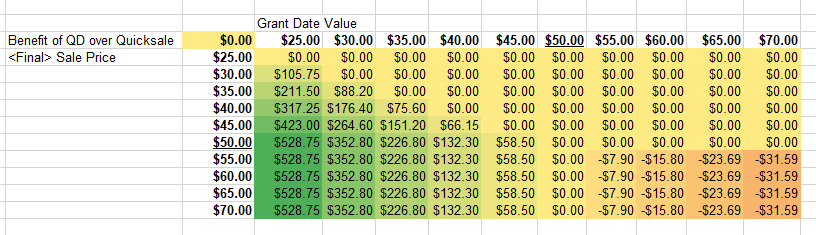

Now we can focus on just the tax differences. Attached is a spreadsheet analyzing the different outcomes for a particular individual making a $100K salary living in Oregon (9% tax on income, STCG, and LTCG) and an INTC purchase date value of $50. It uses "What If" analysis to vary the grant date value and the final sale price, and shows the difference between the taxes paid of Quicksale and a Qualified Distribution (held for >1.5 years).

Conclusions

-

Everything really depends on the difference in price between the grant date value and the purchase date value (let's call it the ESPP period). If the price change over the ESPP period is positive, you will likely have a tax benefit holding to QD. If it's negative (as Ming alluded to), you can actually pay more in taxes! This is because the long-term capital gains from the proceeds from the Quicksale shares are characterized as income if you hold for 1.5 years (QD).

-

As long as your sale price is above the purchase date value ($50), the tax benefits and disadvantages only depend on what happened during that ESPP period above. This means holding beyond the QD date hoping for a better than $50 stock price does not change your outcomes tax-wise, and holding for a worse stock price can both lessen the downsides of a bad 6-month ESPP period and lessen the upsides of a good ESPP period.

-

I don't know the variations in ESPP period prices that INTC will have in the future, but my guess is it will stay around +/- 20% (remember, this is independent of the long-term price trend). From analyzing Robin's historical ESPP data for INTC over the past ~40 years (picture attached), this looks to hold true. This will of course be different for different company sizes and their market segments. The nice thing is that you can pick and choose when to sell your ESPP shares, keeping the good lots and dropping the bad ones if you choose. Most of the time though, it's within $100 of tax difference per ESPP period. What threshold you choose is up to you, but personally $100 ($200 a year) isn't worth the headache for me.

-

This spreadsheet represents about 6 hours of multiple transcription errors and typos on my part, to give you a hint about how long it takes to ramp up on this stuff. Not to mention the different tax forms you'll need to understand somewhat and fill out. You'll have to understand some of them to properly do the taxes for Quicksale, but the rules are a bit simpler to understand.

-

The effect scales linearly with income. (just multiply by 2 for a $200K income). The max ESPP contribution is $25K yearly though, so the benefit has a cap.

-

Any other observations?

There might be errors in the calculations, please let me know if you find any. I cross-referenced them against Robin's ESPP shares taxation spreadsheet and the Intel ESPP page and played around with some simple examples to check the results, which I encourage you to do as well!

I hope this helps your decision making :)

Nolan

ESPP Tax Implications (spreadsheet)

Implementation Notes:

-

LTCG losses are assumed to be deducted from income. (the tax brackets for gains and losses are different)

-

To do What If analysis in Google Sheets, you have to rely on an external plugin that doesn't work correctly half the time. I would highly recommend using Excel if you want to tweak values.

-

Incorporated wash sale tax rules on Quicksale. (can't sell INTC for a loss and re-buy again, so I kept those short term capital gains as a minimum of 0)