ml forex stock algo trading - andyceo/documentation GitHub Wiki

This is the lecture notes for the YouTube playlist

Source: Machine Learning and Pattern Recognition for Algorithmic Forex and Stock Trading: Intro

Link in video's description: Machine Learning and Pattern Recognition for Algorithmic Forex and Stock Trading

Hello and welcome to my tutorial on machine learning and programming for the use of Forex or stock trading and analysis with the programming.

We're going to be using the Python programming language specifically Python 2.7. We're gonna be using Python mainly for its user-friendliness plus it's my programming language of choice, but it also makes a good teaching programming language.

The purpose of the series is to teach you some of the principles to machine learning backtesting statistical analysis and some programming, not to influence your trading decisions. This is my verbal legal statement. This video series is for educational purposes only, and is not an offer or suggestion to deal with any financial markets. How you use this information is completely your responsibility, and I'm not to be held liable. okay, sounds good.

Our goal here is to use very basic machine learning principles to locate actionable trading rules within stocks or Forex. Now I say basic for two reasons.

One, I'm gonna do my best to keep things purposely pretty basic, both mathematicians and stock traders alike. Tend to use big words to purposely make things sound more special than they really are, or maybe make themselves feel better, uh-huh. You're not gonna really find any tie here or at least I'm gonna do my best to keep it simple.

Two, we're going to be doing most of these things by hand. The idea here is to help you all grow in all of those fields mentioned above. There's plenty of pre-made packages for things like support vector machines and neural networks. The problem here, in my opinion, is this doesn't actually teach you anything and it leaves no room for innovation.

Now, using basic machine learning principles to find the algorithm, that's going to be our first step, and that's usually the step most people finish on whether or not they use machine learning. The next question is not only to backtest the algorithm you've found, what's actually going to end up happening is: we're going to wind up with a quote-unquote "live trading algorithm", which basically means it's going to change over time, it will be a dynamic algorithm.

We're also going to do the next, in my opinion, very important step. That's the backtest that method that was used to find that algorithm. So what I mean by this is the following. It's with statistical certainty that if you look at a data set that you can find the best fit line, right? That's nothing special. We see this all the time when someone said: "hey look what I found! You know, here's this back tested strategy and it makes X amount of money!" That's no good, right?

The true test is the forward test, the test on unseen and unaccounted for data. Therefore, if you've created a sort of quote-unquote algorithm to define or derive the best trading strategy, then that algorithm used to find that strategy, right? The method to find that strategy must also have worked in the past against its quote unquote theoretical or actual literal future results, right? So you should also test that strategy against data you've in theory not seen, so you can't actually backtest that method itself. And this is basically to decide whether or not it would have worked to use that method in the past to find an algorithm that you would have also done some back testing on. Anyway, if you're just looking at the data set you found the best algo for that, you know, including the backtesting, that's really cheating, and the likelihood of that algorithm continuing app out in the future is statistically unfavorable.

So, now that we've swallowed that pill, let's go ahead and get all the tools and things that we'll need to do this. So first we are on sentdex.com, which is my website, and all we're here for mostly is a file. I do suggest you guys take a peek around, but that's not what we're here for, I'm not trying to sell you all anything.

What we're going to look for is the zip file. I've got two files located within that zip file and to find that you're gonna go to sentdex.com/GBPUSD.zip, hit enter and that should download a zip file and that zip file is going to contain two files within it. And these are the two files that you'll find: the first files GBPUSD Forex ratio for one day (GBPUSD1d.txt), and the other file the GBPUSD ratio for one month (GBPUSD1m.txt). Obviously you are need to extract this. Once you've extracted it you can open up either of these, so, open this one, and you'll find yourself looking at one day is worth a forex data. I didn't cheat you guys or give you guys nothing to work with. This is actually, as you can see, 62Mb of data. It's bid-ask tick data for this Forex ratio, so it's pretty good data to train on to start with. The next file is a one month of the month May, so you've got a now, you've got a month's worth which is, actually, just over one point one point six million lines here so a lot of lines to work with and a lot of data to work with. So it should be pretty fun to use them. The reason why I split them up is every time we're trying to work with, at least, develop this program using only you know hundred thousand lines versus one million lines is gonna make a sizable difference so that's why we're going to do it that way.

Now back to all the other things that we need. We're going to need a few more things just besides this Forex data, of course. And I also want to stress that even though we are using Forex data, you can do these principles that we're going to go through, can be used obviously for stocks as well. So don't feel like if you're looking to do this with stocks that this isn't going to work out for you.

Now the next most important thing are quite possibly more important than even the tick data is that we go ahead and get Python and we're going to be looking for the Python 2.7. So to get Python go to python.org, then go to download and what you're want to download is not 3.3, you want 2.7.5 and depending on what operating system you have is going to be what you download. If you do have a 64-bit operating system I highly suggest that you download the 64-bit version of Python.

Next we have matplotlib. It is also... well first you get there with matplotlib.org then you will go well it used to be up here but I guess they've moved it on me right here downloads, and then here you get the downloader and again you're going to want to match the download of what version of Python you downloaded or your Windows. Again, I recommend 64-bit if you have a 64-bit system on. If you did download a 64-bit Python you must.

Subsequently, you're also going to need numpy. Now if you followed my rules and you've got a 64-bit version of Python maybe you're wondering why you get a 64-bit version of Python I've said this quite a few and/or quite a few times in most of my videos. The reason you get 64-bit verses 32-bit is because 64-bit has no memory limit... well, it has one but it's huge. 32-bit programs and applications are limited to 2gb of RAM usage maximum. So naturally if you have a relatively large file sizes you're going to max out that 2Gb of RAM pretty easily. That's why I recommend 64. But you'll be able to get through this entire tutorial series and you'll even be able to do some pretty cool stuff even with that two gigabyte limit so don't run away if that's you.

So if you did do that the next thing we need is numpy. What Python allows us to do is program. matplotlib is a package that works with Python that allows us to do graphing. And numpy is a helpful little tool for doing mathematical calculations. To get numpy if you followed everything up to this point and you do have 64-bit, you're going to need to go to this link here. I'll put all these links in the description especially this one, so it's harder to find or at least read (http://www.lfd.uci.net/~gohike/pythonlibs, not working now). What we want here and what this website is is it's a bunch of 64 that's a bunch of installers and it just includes 64-bit versions of a lot of packages that don't naturally or natively offer 64-bit installers so a good example of this is numpy which find here I use a Ctrl-F and type out numpy it's about halfway down the page, and again there is the installers here. If you do have only windows like a 32-bit you can also use the install link here or you can go to like sourceforge.net, I believe, and you can get the other numpy source code or the Installer depending on what kind of computer you're on.

So obviously, you know, if you've got like a Mac or something or if you're on like a Linux distribution something like that you can get in whatever but in the end just make sure you've got Python 2.7, matplotlib and numpy. When you're all done and you've installed all of these things you should be able to go to your Start bar and pull up the python command line. It'll probably be black and not like this but you can customize it so that's just why mine's white. Anyway you should be able to type these following things:

import matplotlib

import numpy

If you can't do those two things like if you go import and you actually spell a numpy right but this and you get this something has gone wrong so if you're having any trouble installing or you've got some sort of error going on feel free to post a comment below and I'll try to help you guys out.

So that's going to conclude the introduction to what we're going to be getting into and hopefully you guys are excited and as always thanks for watching thanks for your support your subscriptions and it's all next time.

@TODO: read youtube comments for that video. All others comments are read already.

Machine learning in any form, including pattern recognition, has of course many uses from voice and facial recognition to medical research. In this case, our question is whether or not we can use pattern recognition to reference previous situations that were similar in pattern. If we can do that, can we then make trades based on what we know happened with those patterns in the past and actually make a profit?

To do this, we're going to completely code everything ourselves. If you happen to enjoy this topic, the next step would be to look into GPU acceleration or threading. We're only going to need Matplotlib (for data visualization) and some NumPy (for number crunching), and the rest is up to us.

Python is naturally a single-threaded language, meaning each script will only use a single cpu (usually this means it uses a single cpu core, and sometimes even just half or a quarter, or worse, of that core).

This is why programs in Python may take a while to computer something, yet your processing might only be 5% and RAM 10%.

To learn more about threading, you can view the threading tutorial on this site.

The easiest way to get these modules nowadays is to use pip install.

Don't know what pip is or how to install modules?

Pip is probably the easiest way to install packages. Once you install Python, you should be able to open your command prompt, like cmd.exe on windows, or bash on linux, and type:

pip install numpy

pip install matplotlib

Having trouble still? No problem, there's a tutorial for that: pip install Python modules tutorial.

If you're still having trouble, feel free to contact us, using the contact in the footer of this website.

Finally, you will need: Forex Tick Dataset For This Tutorial

The plan is to take a group of prices in a time frame, and convert them to percent change in an effort to normalize the data. Let's say we take 50 consecutive price points for the sake of explanation. What we'll do is map this pattern into memory, move forward one price point, and re-map the pattern. For each pattern that we map into memory, we then want to leap forward a bit, say, 10 price points, and log where the price is at that point. We then map this "outcome" to the pattern and continue. Every pattern has its result.

Next, we take the current pattern, and compare it to all previous patterns. What we'll do is compare the percent similarity to all previous patterns. If their percent similarity is more than a certain threshold, then we're going to consider it. From here, maybe we have 20-30 comparable patterns from history. With these similar patterns, we can then aggregate all of their outcomes, and come up with an estimated "average" outcome. With that average outcome, if it is very favorable, then we might initiate a buy. If the outcome is not favorable, maybe we sell, or short.

For visualization, here's an example: pattern recognition tutorial

{kind=link}

In the above example, the predicted average pattern is to go up, so we might initiate a buy.

This series will not end with you having any sort of get-rich-quick algorithm. There are a few known bugs with this program, and the chances of you being able to execute trades fast enough with this tick data is unlikely, unless you are a bank. The goal here is to show you just how easy and basic pattern recognition is. As long as you have some basic Python programming knowledge, you should be able to follow along.

The next tutorial: Quick look at our data

In this video, we are looking at and displaying the data that we are working with, and matplotlib.

Source: Machine Learning and Pattern Recognition for Algorithmic Forex and Stock Trading: Intro

Tutorial page: Quick Look at our Data

Hello and welcome to part two of machine learning and pattern recognition for use with stocks and forex trading. Now you might not realize it, but you've actually just made a huge accomplishment already, and that's that you're viewing part two.

You look at a lot of series on the internet especially tougher ones. It's usually at least a 25-40 percent drop off between part 1 and part 2, right, so you've already taken the initiative and you're already ahead and probably what's going to turn out to be of at least 25% of everyone else. So congratulations on being serious! If you continue devoting some time, soon you'll be in that top 1 to 5% and you'll have some cool new skills.

Also to give you a bit of a teaser: you're only just a few videos away from coding pattern recognition. They'd find something like this: this blue line is the patterning question and all these other lines are historical patterns that followed a closed pattern to this one and then what we'll end up doing is predicting the future results based on these past pattern results. Definitely something to be looking forward to, that's really only a few videos away.

The first thing that we really want to do is going to plot out the data that we have, so we can actually see what we're working with and see what our goals are.

Also be useful just to get comfortable with matplotlib we're going to be using at. So what we're going to run through is: opening up this data and looking at the data that we have first.

So we're going to need a few imports and that's going to be:

import matplotlib

and then we're going to go ahead and import some other stuff even though we've imported the

full matplotlib we also want to import various things as specific things, so we're also going to do:

import matplotlib.pyplot as plt

import matplotlib.ticker as mticker

import matplotlib dates as mdates

Finally we're going to

import numpy as np

Now we're going to do a function is going to be graphRawFX() and under here we're going to have a numpy open up this text file and create numpy array for us. So we're going to say:

date, bid, ask = np.loadtxt('GBPUSD1d.txt', unpack=True, delimiter=','

converters={0: mdates.strpdate2num('%Y%m%d%H%M%S')})

This is going to load up any text file you have. It can also do arrays even though it is called loadtxt() and the text we want to load up is going to be GBPUSD1d.txt. So if you got those files that I got or you got you can download from sentdex.com. If you take the zip, unzip it and there's two there should be two text files in there, one is GBPUSD one day and one is GBPUSD one month. Make sure both of those text files are in the same directory as this script. So not to folder the both text files. So if you just have the folder it's not going to find it, so you would need to put the folder in front. so just keep that in mind. I'm going to say unpack=True, and the delimiter of this file is a comma, and the converters (this is so we can convert a datestamp to plotting dates) and that's going to be the zeroth element, so the first element in there, and so let me just pull up the file real quick. This is our gbp/usd one day text file so you've got the datestamp and then bid-ask and here we can see year and then 05 is the month, 01 is the day and then hours minutes seconds. So we come back over here and our converters is going to be the zeroth element, wow do we want to convert this? use mdates and then we're going to use strpdate2num so strip date to num, and then in parentheses you give it the format that this is in, and you do it with percent and then a character that denotes whatever that is. So first we'll do %Y that's for a full year, then we do %m%d, so: month, day in number format; then %H for hours, %M%S. That's the whole thing. If you've had dashes or something in a date you would also put those in there, but again, we don't really have that it's just a straight stamp. So that's the conversion that we must make.

And come down here.. now the next thing we want to do is plot this: so we're going to define the figure that we're going to plot on and our figsize will be ten by seven:

fig = plt.figure(figsize(10,7))

Next, we're going to do a ax1 equals plt.subplot2grid(), and within here the grid we'll make is just a forty, forty, size we'll start the plot at the zero, zero, rawspan for 40, and colspan also equal forty:

ax1 = plt.subplot2grid((40, 40), (0, 0), rowspan=40, colspan=40)

If I'm going too fast at this point for you guys as far as defining how to make this chart then I highly suggest you check out the Python charting tutorial. I've got a whole series on all this stuff and it goes and way further depth than this. So if you do feel like you're lost, I highly suggest watch that, otherwise just kind of copy what I'm doing because honestly this part is not the main part of this series. We are just trying to display the data and we will continue displaying data. But this isn't really integral to the entire understanding of machine learning.

The next thing we want to do is to plot a date and bid:

ax1.plot(date, bid)

Then also we want to plot the date, ask:

ax1.plot(date, ask)

Then what we want to do is format the x-axis so it's in like date format, right? So:

ax1.xaxis.set_major_formatter(mdates.DateFormatter('%Y-%m-%d %H:%M:%S'))

Date format: now you can choose anything you want so let's make this date a little bit prettier than it wasn't on the first time around, so: %Y-%m-%d %H:%M:%S.

Next the other thing we're going to do is:

plt.grid(True)

and

plt.show()

It's going to be kind of an ugly looking x- and y-axes ticks but you'll get what I'm saying in a minute so let's just bring this up and so run it, after you've saved of course.

It should pop up for you guys now and here is the data. There's a couple of things that are just kind of ugly about this data, right? You've got the date stamps are kind of running over each other, and the values over here are kind of being like converted because they have a lot of zeros and stick data and this data goes way past a pip, right? I think it goes to places past a typical pip.

Anyway this is our data, this is a one day of bid-ask tick data. The only really thing I wanted you guys to see is that it's, you know, we've got a fairly volatile day and overall at least on this day the data is rising but I believe in overall, true overall, we could bring up that data and I believe overall and for the month of May it was actually falling.

I got this error because it never we misspelled date formatter... Anyway that's the basic chart, that's the basic data that we're going to be dealing with and one of the interesting things about bid-ask... let me bring it back up again real quick... as you can see, the gap or this what's known as a spread and you can almost see pretty much every time the spread gets wide right it's either going to fall or go up right? Volatility is pretty much attracted to that spread which makes sense.

If more people like less people are willing to sell and that gap starts why not well it's probably the case that the stuff is going to go up or down same thing when it's crunches up right like here you've got scrunch up and like there's really no gap here because everyone's like chasing it, right? So there's also some pretty cool stuff that you can do with spread. However, we're not really going to be dealing with spread at least in the initial videos, we're going to be dealing with price change but the option is there for spread. In the next video I'm going to show you one more thing about spread and then we're actually going to continue on moving away from spread or at least moving without spread. But spread is definitely something you'll want to consider in the future if you do decide to go down this quant trading route.

So anyways that's going to include the second video in the third video let's we're going to at least show you a few more things about charting and we'll put up an interesting graph with spread and then from there we'll begin working on some patterns, setting up those and then the machine recognition of those patterns definitely some cool stuff to look forward to. If you're not subscribed I highly suggest you subscribe. Not going to release the series all at once so they'll just be coming out as I end up making the videos so if you're subscribed you should get something in your email or something that tells you that "hey I've got another video" or you can just keep checking back. Anyway that's going to include the video as always.

Thanks for watching thanks for all the support and subscriptions and until next!

In this video, we are briefly taking a closer look into the bid-ask spread before diving into pattern recognition.

Source: Machine Learning and Pattern Recognition for Stocks and Forex Part 3

Tutorial page: Basics

What's going on guys?! Welcome to part three of machine learning and pattern recognition for use with stock in forex trading, where we left off and we're just graphing up our data. There's a few ugly parts to the data so we're gonna fix those things, and then one more thing I'm going to show you is just another representation of that spread because, again, I feel guilty because I'm pretty sure we're gonna leave spread out of this entire series so just want to point out spread to you before we end up going down this really really long path that probably won't ever get back to spreads, so anyway let's go ahead and do some stuff with this plot and then we'll be on our way.

So the first thing that we did really only change we made to just the raw plot, right? I guess, we changed the figure size, and then we did the dates, but we haven't really done anything else. So there's a couple other things that we probably ought to do and just for displaying this kind of tick data, the first thing that we're going to do is once we've arranged this date. The next thing that I think we ought to do is kind of curve or angle the date so we can go:

for label in ax1.xaxis.get_ticklabels()

label.set_rotation(45) # 45 degrees

Next thing that we really want to do is fix member on the y-axis. How it was like, I don't know, the numbers right? it was doing like a +1.whatever we kind of want that to go away since that just looks ugly there's no reason before what we kind of want to see these decimals. So because it does that for us for a good reason, so most of the time you don't really care about really long decimals, but in this case this is one of those times where we do care. So what we're gonna do is do:

plt.gca().get_yaxis().get_major_formatter().set_useOffset(False) # turn that to false so it doesn't do that to us

So now let's just see where we are real quick and make sure we didn't do anything wrong or typo. It's highly likely that I type typos it's hard to type and talk. Sure enough I did: I put a comma right here so you'd dot if you were actually following me make sure you put that dot there and I get this stupid air I did that. Now let's try again see if we've got any other errors... Yeah, we didn't! okay so here's what we got right now obviously the dates kind of thing go out there, but again this is really just one day where the data, so doesn't matter too much. Plus if you see down in the bottom right where you cover you can see the time and the value so it's not a huge deal, but I'll show you guys how to fix that just in case you care. So anyway we close out of that that's looking good for now. Let me hit this gonna give me an error... okay so to make space for the bottom what we can do is use this subplots_adjust():

plt.subplots_adjust(bottom=.23)

Again, that's another thing that's covered pretty well in that other video. It's pretty much all of this stuff. If you want to know more about formatting charts, you can check that out. But again, that's not really the focus of this tutorial since I've already covered it, so I don't want to cover the same stuff especially for the people who have already watched those other videos.

So the last thing I really want to do is show you guys a representation of that spread and so if you did watch the other video, it'll be a lot like how we did volume, right? So what we're going to do is we're gonna say:

ax1_2 = ax1.twinx()

ax1_2.fill_between(date, 0, (ask-bid), facecolor='g', alpha=.3)

And what I wanna fill between? Date first then zero, that's like the minimum that it will fill under and then ask - bid. (Ask price) - (bid price) - otherwise known as the spread.

ax1_2.plot(date, (ask-bid))

ax1_2.set_ylim(0, 3 * ask.max())

Then we'll just give it a face color of green and an alpha of 0.3. And that should be it. We show a pretty decent looking chart at this point so save that and run it.

Obviously if you're not totally new to Python to run the function. You gotta type in you know graphRawFX() and enter.

You can actually see this down here is the spread size basically. You can see some cool stuff with that spread size. Anyway, just something I wanted to show you guys since we did have bid-ask tick data here that you can do with that data.

So anyway we're going to close out of this out. That's going to conclude the third video in the machine learning for Forex and stock trading.

In the next video we're going to start building up our pattern finder, so we're going to go through the text file and start looking for patterns.

As always thanks for watching and thanks for your support of subscriptions and until next.

NOTE: local graph is not the same as in the video: local version have no some kind of histogram effect for the spread.

This video has us beginning to build our comparison ability, which will be used in pattern recognition. This part could be done in a logarithmic fashion, but we're going to try to keep things as simple as possible!

Source: Percent Change: Machine Learning for Automated Trading in Forex and Stocks Part 4

Tutorial page: Percent Change

Hello everybody and welcome to part 4 of machine learning for Forex and stock trading analysis! Now that we've seen our data let's actually talk about our goals, what we want to do here. Generally with machine learning everything is going to boil down to actually machine classification. So with quant analysis gentlemen the first few things that you're taught are these quote-unquote "patterns": head shoulders teacup whatever else silly names that they've got... There's tons of these patterns, so what's a theory behind these patterns?

Well, the idea is that prices of stocks or forex ratios are a direct reflection of psychology of the people trading. So the traders, either people or computers (I guess you wouldn't want to call it totally "psychology" but maybe the variables that built up to make that pattern), so the people or computers they're making decisions based on a bunch of these variables and the theory is when the same variables present themselves again you'll get a similar pattern. So you'll get a repeat of actions that create that similar pattern and then the outcome as well is likely to be very similar. The further we move away from that pattern, the higher likelihood of similarity of the outcome changing, but you don't have to move too far away from the pattern, really, you just need to move far away enough for you to actually execute a trade and that's all you really need. And, really, with quant analysis, algorithmic trading or on automatic trading that really doesn't need to be too far out since the computer can actually execute the trade pretty quick faster than you will be able to. At least our initial goals are:

-

Create a machine learned batch of what will end up being quite possibly millions of algorithms and the results, which is going to be used to predict future outcomes compared to the outcomes in the past of these exact same algorithms. Now obviously as time goes on we can cut out some old algorithms if you don't want to use the same algorithm from years ago, or you might not want to or maybe you want to weight it differently. But as you're going to find out as we get through this, there's a whole bunch of options that we can do. So we're going to kind of put them on the table. We won't get too in-depth, otherwise, we would never make progress, but, you can imagine.

-

Actually test this basic theory. So the beauty of machine learning is this notion of what's called data snooping. Data snooping is basically like making new inferences after looking at your data, so with machine learning data snooping is actually built-in. On the other side, if you don't really look too in-depth into what machine learning is actually doing, you might actually accuse it of: "Well, that's just machine learning and that's no good", right? But what you're missing is that data snooping is not only built-in, but it's actually accounted for. It's really great.

So our whole system here is really built on the inference of pattern recognition, not the algorithms itself, so if patterns changed in new data, that's actually already built in and is done by programming, that's done before we've even seen the results. This allows researchers to actually get the best of both worlds, while avoiding some of the pitfalls of data snooping.

So what this is going to let us do is it allows backtesting to actually serve a really truthful and accurate purpose. If our machine learned live algorithm passes the backtest in every sense of the word: using historical data and only using historical patterns is it still accurate as we move forward?

If the answer to that is actually "yes", then it's highly likely to continue performing well in the future as well, because it's actually the machine learned patterns that are paying out, not the exact pattern as it were profitable at the time. So really it's confirming the hypothesis. We have an actual reason why we think this might work: we're going to put it in action and if it does confirm, that it actually confirms the hypothesis.

That's what we're really looking for, unlike finding like some sort of mathematical equation for no reason. You just kind of kept flipping around variables until you found one and backtesting it and: "Holy moley we got great results! This is going to make me bank!" No, that's unlikely.

What we're going to do is take a range of data in succession. To start, we keep it really simple and so simple that it literally will be stupid, but we're going to do it. We create a pattern with that data. The sense of the reason why I say it's stupid is we're going to use a range of 10. Don't forget we're using tick data, so a range of 10 in this tick data is really under most likely to be less than 10 seconds of a timeframe.

Most people aren't going to have bid-ask tick data, they're going to have more like bar data: open, high, low, close data and it might be for one minute open, high, low, close, something like that, but not everyone is going to have this bid-ask tick data, but if you pay for it, you can actually get that data stream, anyway, beside the point there bright chance be too short of a range, but luckily, something like this, same thing with percent similarity which we'll find out way later on, and even the time length, all of this stuff can be machine learned to find the best of everything at the time.

And again, it's not data snooping, it's just built in the machine, there's no new programming that will take effect, it will just continue and continuously not only find the best patterns, but it will find the best lengths of pattern to care about, how long of a timeframe do we care and how similar will we require these patterns.

Not in this video, otherwise we would literally not do anything in this video, probably a few more videos away we'll get it in a little bit more detail about why that matters and why we want to find out how close. Wouldn't we want like a 100% match of patterns and all this stuff? And, no, the answer really is quite firmly "no".

We're going to take this range of data in succession and create a pattern with it, and the way that we're going to do it is with percent change. We want to normalize the data as best as we can, so that we can use it everywhere, even if the price has changed that pattern. So if you just had a pattern of let's say $100, on $1, on $3, on $2 that pattern if you required it to be like that: when it matched the $10 and $10 and twenty cents or whatever that pattern once I just said, it wouldn't match even though it graphically it would be identical.

So we want to normalize that data. The preferred method properly normalize data is to do it logarithmically, but what we're going to do is to use percent changes to keep it as simple as possible. And the next thing to consider is how we're going to do this percent change now? The way that we're going to do it is a forward percent change from starting point. This means the longer that the pattern is, the more likely the end is to be less similar than the beginning, but the actual direction in movements of the pattern will be very similar. So this can be useful since some patterns might take more time to react to a movement than others and we want to build up, in my opinion, to be most accurate.

But what we actually want is for the end to predict the future, and so if you wanted the end to be more accurate you would do a reverse percent change. So from the last point, what is the percent change the point #9 to point #8, 7, 6 point, whatever. Or you could do a point to point percent change and really make some stuff pretty stringent. If you do point to point percent change you run the risk of that pattern doing some pretty wild, like it can be very different visually even though you might not think, so it can wind up going in a completely different direction. So I don't think we want to do that.

Now, anyway, like I said before, all this stuff can be changed there's already a lot of variables and trust me, when it comes to variables we're going to be very, very busy. Some of them, luckily, can be machine learned very easily, the other ones can be machine learned very difficult.

Forward starting point: this means that first we need to store a bunch of patterns in the percent change format. In reality and in our backtest, that will actually mimic this, your patterns can only obviously come from the past, so when we do backtest it we won't be able to be like: "Well this pattern from May, 1 looks a lot like this pattern on May 8th!" Hey, you can't do that! So then what we do is compare the current pattern to similar patterns in the past using this percent change, and, again, this can be done logarithmically, but it might be better that way, the goal here is to keep things as simple as possible. And then what we can do is if when we find similar patterns, we can look at what was the outcome of those similar patterns in the past.

So let's actually code something now. The first thing we need a code is a percent change function. We could do this by hand every time, but we're going to be doing a lot of percent change, so it would just make sense to go ahead and shorthand this for ourselves, so we'll want to do this.

So we're going to define percentChange() and in the parameters we want a start point and a current point, from what to what are we going to do percent change to:

def percentChange(startPoint, currentPoint):

return ((currentPoint - startPoint) / startPoint) * 100

Percent change is: ((new - the old) / the old) times 100. I see people do a different form of percent change and it really bothers me and there's good reason for it sometimes but not now.

The next thing that we want to do is actually program a function that is going to use percent change and just go through everything and make all these percent change patterns. That's what we're going to be doing in the next video so you're welcome for a percentage change and a bunch of talking! Anyway, hopefully that sounds interesting to you guys hope you guys are excited for the future videos.

As always, thanks for watching!

Welcome to part 4 of machine learning for forex and stock trading and analysis.

Now that we've seen our data, let's talk about our goals.

Generally, with machine learning, everything boils down to actually: Machine Classification.

With quant analysis, generally the first few things you are taught are "patterns" Head and shoulders, teacup, and whatever else.

So what is the theory behind these patterns? The idea is that the prices of stocks or various forex ratios are a direct reflection of the psychology of the people trading, ie: the traders (either people or computers) are making decisions, based on a bunch of variables. The theory is that, when those same variables present themselves again, we get a repeat of actions that creates a similar "pattern," then the outcome as well is likely to be similar, because the variables are almost the same.

So what we're going to do here is

-

Create a machine learned batch of what will end up being millions of patterns with their results, which can be used to predict future outcomes.

-

Test this.

You may have learned a few simple patterns, but everyone knows these. What if you could know every pattern in history? Pretty hard for you to remember them all, but not too hard for a computer.

Our entire system is really built on the inference of pattern recognition, so if patterns change due to new data, that's really built in and is done by programming that was done before results.

This allows backtesting to actually serve a very truthful and accurate purpose. If a machine learned live algo passes the back test, it is highly likely to continue performing well in the future, not because it passed a back test, but because our hypothesis and entire model passed the backtest... unlike finding the best algo at the time and backtesting for great results.

With that, what we will do is take a range of data in succession, and create a pattern with it. How we're going to do this is going to be with % change.

We want to have the data normalized as best we can, so it can be used no matter what the price was. We're just going to use a succession of % change for it.

To start, we'll do forward percent change, from starting point. This means, the longer the pattern, the more likely the END is to be less similar, but the actual direction of the pattern will be more similar. This can be useful, since some patterns might take more time to react than others, and we want the build up to be most accurate, but we might actually prefer the end to be more accurate in the future, so we could do reverse percent change. We can also do a point-to-point percent change as well. Trust me, when it comes to variables, we're going to be very busy.

Now what that means is first we just need to store a bunch of patterns, in their percent change format.

Then, what we'll do to compare patterns is how similar the % changes are.

def percentChange(startPoint,currentPoint):

return ((currentPoint-startPoint)/startPoint)*100.00

This video has us beginning to build our comparison ability, which will be used in pattern recognition. This part could be done in a logarithmic fashion, but we're going to try to keep things as simple as possible!

Source: Finding Patterns: Machine Learning for Automated Trading in Forex and Stocks Part 5

Tutorial page: Finding Patterns

Hello and welcome to part 5 of machine learning for the use of algorithmic trading, where we left off from a this percent change function. We haven't actually tested this percent change function. One of the main issues with this is going to be that it's not going to be willing to work with whole numbers and give us a decent output so for example let me just show you:

percentChange()

...talking about Python's 2.7 integer division, import division or add decimal point...

... fixing percentChange() function with float and adding decimal point...

Now the next thing that we want to do is actually make this pattern finder so what we're gonna call it is actually a patternFinder() I know you can see that name coming I try to choose really weird names.

Now the first thing that we need to do is where are we going to look for these patterns. Well probably the best place to look will be in the file so let's just go ahead and: put date, bid, ask = ... to global variables.

Also keep in mind now that we've moved this if we decided to manipulate these variables at all down here we would need to global <variable>. Just keep it in mind. As long as you don't manipulate the variables themselves it'll be fun.

So, patternFinder(). First thing we want to do is let's simplify this, because as you probably starting to see weird. As we go on, there's gonna be a lot of variables here. And as long as we continue on with bid-ask kind of prices, it's going to get really really messy and we might not ever actually finish this series. So the best thing for us to do is to just make it a simple average of the average line. To do that we do: avgLine = (bid+ask) / 2.

This is just going to average bid and ask, so to give us perfectly the middle spot of between bid and ask. Now you can see we've thrown away spread and why I just wanted to point it out to you guys initially, because we're not going to be touching spread for quite a while if at all.

Next, we're going to look for patterns in here and then, as we look for all these patterns, the next thing we want to do is: for every pattern we find we want to know what the outcome of that pattern is.

So with that we're gonna to say: x = len(avgLine). After we find that pattern, we're gonna look 20 to 30 patterns into the future, we're going to look for the range of between 20 and 30 and we're gonna average the outcome, like between 20 and 30 what's the average price. So from there we'll get the average outcome between 20 and 30 and this is the average number in the future that we can kind of hope to achieve.

If it only hits like this number for split second, we won't want to call that the outcome. So, instead, we're gonna take a range of numbers, average them and say: "okay, this is the outcome". Because of that, we're gonna look also 30 digits in the future and we're gonna use x as like a counter so I guess before I do what I was going to do I'll show you why.

Next thing I want to do is: y is going to be the starting points that we use. So y=11. Even though I really think it ought to be 10, I will just call it 11 just to be safe and just ignore the first point. Next: while y < x:. The reason why we're going to add a while loop is we're going to make it into a counter, every pattern will do plus one and log that pattern, while y is greater than x. Now you can understand why: because we're going to make this into a counter, eventually, we're gonna hit the length of average line and then when we go to look for what happened in the future, it's not going to be available. That's why we need to throw in a minus 30 here: x = len(avgLine) - 30.

Make sure you do that: x equals the length of average line minus 30, so it will stop at the minus thirtieth x basically. That way we can still look into the future.

In the loop we want to say: p1 = percentChange(avgLine[y-10], avgLine[y-9]). Starting point is avgLine[y-10], end point is avgLine[y-9].

So for every point (along this way like p1 will just be literally point 1 in this pattern), so for every point along the way the starting point will remain the same (as I said we could change this but for now we will not) and so this y-10 will always be the same. But, we're gonna change the ending part. The easiest way to do this is, since we have 10 points and a lot of this will be the same, we'll just paste. ...copy and paste p1, editing p index and end point in percentChange()... Now so that's point 1, 2, 3 etc.

The next thing we want to do is we want to say what is the outcome range.

And that's going to be average line and the range of outcomes is y+20 all the way to y+30 so basically the the 10 numbers between, whatever y is at the time, plus 20 all the way to y plus 30, so this produces an array of 10 points: outcomeRange = avgLine[y + 20:y + 30]

Then what we want to do is what's our currentPoint = averageLine[y]. Not really need this in the future but we'll use that for now and just for printing out function.

Now we want to average the outcome of this, so for now we'll just print that out, an we're going to use lambda to do this. If you don't quite follow I do have a tutorial on lambda. Otherwise, just copy what I do, it's just a really quick way for us to average:

print(reduce(lambda x, y: x + y, outcomeRange) / len(outcomeRange))

It's basically adds everything together so for every x and y it's just gonna add them together within outcomeRange and then divide it by the length of the outcomeRange, otherwise known as average.

Next, print currentPoint, little spacer and then print p1, p2, p3, p4, p5, p6, p7, p8, p9, and p10. And finally do we have sleep? No. So go up to the top and import time. If you're gonna copy me: I'm just gonna make something that pauses with sleep, so we'll do time.sleep(whatever).

This is basically the storage of one pattern. If we leave this like this y will always be less than x and we will just get a bunch of the same pattern. So what we need to do at the end of this function, and I shall put it before the sleep, just put y += 1. This just is a shorthand way to add one to the variable y.

Let's go ahead and save this and let's run patternFinder() and see if everything is worked. It should take a second to load on start because it's loading up GBPUSD1d.txt into your RAM and creating these arrays. So that's being loaded into your memory, so every time you load it's going to take some time, and that's why we global this variable because otherwise if you put it like, maybe, down here, it would be doing that a lot.

Anyway, more on that later, excites another thing that we'll run into in a little bit, so we want to run is patternFinder(), enter. And sure enough, basically, what we've done is

we've printed the outcome first so the outcome you can actually see the outcome is slightly higher than the current point that we're on. Even though this is just really it's a pattern. In theory this pattern is a pattern of profit for in the tone of... not even a full pip, like a half a pip.

Anyway we can see here: minus a tiny percent, minus a tiny percent, minus, minus, minus... might actually a lot of minus percentage. But anyway in the future we can see that after all of these little minus percentage and if you plot this up, it would make a pattern of some sort. We can see in the future it does produce a half a pip, or a little bit less, but basically you have a pip and so a little bit of money, but, anyway that's one pattern.

Now what we're gonna want to do is begin a whole storage of all of these patterns and then we can start to compare against patterns. Anyway, that's the storage of a single pattern, and in the next video we'll continue building of this.

As always thanks for watching thanks for all the support and subscriptions and until next time!

Lecture 06. Pattern Finding and Storing: Machine Learning for Algorithmic Trading in Forex and Stocks Part 6

In this video, we are finding and storing patterns to be later used in the pattern recognition.

Source: Pattern Finding and Storing: Machine Learning for Algorithmic Trading in Forex and Stocks Part 6

Tutorial page: Storing Patterns

Hello and welcome to these sixth part in the tutorial series of machine learning applied to stocks and Forex! Where we left off? We were making this patternFinder() basically and we printed it out. We're not actually saving the pattern or anything, so now what we actually want to do is begin saving this pattern. So what we want to do is: come up here and create an empty global array, actually 2 empty global arrays. First one we want is patternAr = [] for pattern array. That'll be empty for now. What this is going to do is as we run patternFinder(), every pattern will get stored into the pattern array.

Subsequently the next thing we're gonna do is create a performance array performanceAr = [] where we store the outcome which was an average of in the future in the next twenty to thirty points what was the average price at the time, so we're calling that the outcome, so we're also going to store that to that performance array and in these two arrays each value in the array will have the same index number as its partner.

Now you might think well why aren't we making a dictionary out of this? And it would have been nice to make a dictionary or you can make like a multi-dimensional array or something otherwise known as a dictionary, usually... But the issue with the dictionary is what we really needed was the key to be the pattern array, because what we're gonna do is: when we find a pattern, we find a similar pattern and then we wanted to compare that pattern and see what the outcomes were. But the issue was you can't have an array as the key. If you have no idea what a dictionary is, don't worry about it, I guess, but for anybody that does know what a dictionary is probably wondering why we're not doing that. So, you can have an array as the key to the dictionary, it would have to be the performance value, but you can't, this is the kicker! You can't have an identical key in the dictionary. You can have identical values, you could have different keys equal the same thing but you can't have identical keys. So you stick, when you go to define that key you would overwrite the most like the other key, and the problem with this is you would be overriding possibly better results like a more accurate pattern might end up getting more overwritten. Anyway it would be a huge mistake to do it, so we're not going to do that, we're just going to make two arrays.

So change the name patternFinder() to patternStorage(), because actually soon we'll actually make a pattern finder and that'll make more sense to call it pattern finder. That's what it doing, it's storing patterns.

Usually in something like machine learning type of script or a script that's doing a lot of calculations you want to have processing time: patStartTime = time.time(), so that will store whatever time it is currently and then, at the very end of this script: patEndTime = time.time() And then at the end we'll subtract the two. Thus you can find out how long took the storage of patterns, so this way you can start to find inefficiencies in your script.

...then, create avgOutcome in try / except block...

Reason why we do this is with doing a percent change of a percent change and so this can give us especially... well I won't get into the maths, but well you can wind up with a negative infinity percent change. So in case of exceptions, just in case, we've type out something and then also if this does happen, we'll just say the avgOutcome=0.

Remember how this basically the average outcome created: a number with the digit of that outcome was. That's no good, we need it to actually be a percent change as well. Again, we need to normalize everything. Probably this is the most accurate representation of using percent change or a logarithm: futureOutcome = percentChange(currentPoint, avgOutcome). Keep in mind the average outcome can be zero, so that gives us a possibility of a division by zero and also all kinds of interesting stuff.

...change the percentChange() to correctly calculate the cases from negative startPoint to positive startPoint. Examples: percentChange(-10, 20)=300, percentChange(10, -20)=-300...

You need those absolute value bars (abs() in this case) but it's basically what absolute value bars does and written that. We need that there as well because we will have percentChange() using a negative numbers when we compare... not only future outcome can have it but then also when we're start comparing formula or comparing patterns we're going to see in a lot.

We need to append the pattern to this patternAr, also we need something that's like pattern. So while y < x: we start with an empty pattern, and then do pattern.append() and we need to start appending all this pattern, obviously need to append it in the order. Now we've got a pattern appended one to ten, so it made an array, so this pattern is now an array of percent changes and now, we need to do patternAr.append(pattern) Subsequently, performanceAr.append(futureOutcome).

Just to make sure we've done everything these lengths ought to be the same. so we'll print the length of patternAr, print the length of performanceAr and then also we want to print the time it took to store these patterns: print('Pattern storage took:', patEndTime - patStartTime, 'seconds'). Save that and run this and make sure we are indeed storing patterns and it will only store all the patterns found in one day, but, I believe, that was already like... I forget how long that this file is, but it's a pretty long file, so should have quite a few patterns.

So we found 61971 patterns, 61971 outcomes to those patterns and the storage of all of those patterns, the time it took to run through this entire file took 2.12 seconds so if you were to use fresh data and run through the month, that would be 30 days we take about a minute, in theory, to do it all, probably, a little bit less, we can talk about that later.

Sure enough looks like we've stored all of these patterns. We've done it successfully, so our pattern storage works. Actually we could test this and say: patternAr[5], and see pattern of percent change in array, 5 and then our performanceAr[5] print the outcome of that array and it's a positive.

Conclude this video on the pattern storage function here. In the next video what we're going to do is creating our pattern recognition. We're going to: store all the patterns, find the most recent pattern and then find previous patterns that are very similar to the current pattern. I'm going to make another function, and it's going to be our actual pattern recognition function. Hopefully that sounds interesting to you guys.

As always, thanks for watching, thanks for the support, the subscriptions and until next!

-

Question: I have a question that I must have missed watching the videos. On line outcomeRange = avgLine[y+20:y+30], why did you choose 20 and 30. Our first pattern is avgline[1:10], and the performance or avgOutcome is the percent change of our currentPoint or avgLine[10] to the average of avgLine[30:40]. Why do we compare so far into the future? Or why wouldnt we check for percentage change of the next 10 elements?

- Answers: You're free to choose what you want. The reason I chose it: It's y, which is the last point, plus 20 points out, to 30 points out. Then we average this to find the average "outcome" price. The idea to compare it to the average of where price ended up after our pattern, in a time frame where a trade could plausibly be executed. It's possible somewhere along the lines I chose bad numbers. I literally programmed this series as I went, which is discussed in the end a bit more in detail. Feel free to change things as you see fit, there are a lot of variables to play with in this series, and I just arbitrarily picked values. Hope that helps.

-

Question: So length of the pattern and how far in the future can be adjusted to find the best possible combination. Thanks a lot, it is a great tutorial.

- Answer: To name a few, yep. In the end quite a few of the variables are discussed. Glad you are enjoying the tutorial! Was a lot of fun making it and worked out better than expected.

- Authors' CPU is i7 3930k.

-

Question: Is the stored patterns same as features in ML jargon?

- Answer: The stored patterns are more like featuresets, and each % change is a feature.

In this video, we are are locating the latest pattern, in order to compare it to the previous ones for pattern recognition.

Source: Current Pattern: Machine Learning for Algorithmic Trading in Forex and Stocks

Tutorial page: Current Pattern

Hello and welcome to these seventh video in the tutorial series of machine learning for use with stocks and Forex algo trading! We were storing a whole bunch of patterns into an array and basically into memory and now we actually begin the pattern recognition part of this, basically, what is our current pattern that we have right now.

Make another function def patternRecognition(). Here we're going to make an empty array patForRec = [], which basically stands for "pattern for recognition". What is the pattern in question?. For this, make a bunch of variables and it's going to be cp for current pattern, cp1 = percentChange(avgLine[-11], avgLine[-10]) for current pattern for 1, basically. Again we use our percent change calculation, which this rely on the average line. To determine our current position within the pattern, we can use negative indexing. By using -1, we refer to the last element in the array. Similarly, if we used -11, it would point to the tenth-to-last element. So, our starting point is -11, and the current point is -10. For others cps, we copy and change that string like: cp2 = percentChange(avgLine[-11], avgLine[-9]), etc. The percent change will be calculated from a specific point, following a kind of backward format here. Starting from this point -11, the values are as follows: 1, 2, 3, 4, 5, 6, 7, and so on. The percent change will be determined using the same format as our pattern storage. Now, store this so patForRec.append(cp1) and copy-paste with changes. Better way to do this with a for loop or a while loop but again we're trying to keep this pretty simple.

Just to make sure we did everything right do. print(patForRec). Save that and run this pattern recognition function. avgLine is not defined. Move avgLine from patternStorage() to global.

This is our current pattern in question. In the next video, our focus will be on comparing this pattern with previous ones stored in our memory. Stay tuned for that!

As always thanks for watching!

- sentdex comment: Personally, I am more of a fundamental investor myself. I just enjoy programming and machine learning. This whole series here doesn't use sentiment analysis at all. For my website, that is pure sentiment, and that is my main focus in business. As for books, I don't know. Quant traders are an elusive bunch. The ones that make money don't talk much about how they do it. The way I personally learn is to be like a sponge and absorb all i can, mostly from online documents. Best wishes!

-

Question: why did we subtracted 30? in this code

x = len(avgLine)-30-

Answer: For a given current point

y, he want to use the pattern of 10 previous points (fromy-9toy) to predict the future outcomes (pointy+20toy+30). He usex = len(avgLine)-30so that the while loop does not go over the total length of the data.

-

Answer: For a given current point

-

Question: why we have taken y=11 is it fixed?

- Answer: Since he consider the pattern of 10 previous points of a given current point, he picked the starting y=11 so that it has exactly 10 previous points

Lecture 08. Predicting outcomes with Pattern Recognition: Machine Learning for Algorithmic Trading p. 8

Using previous pattern outcomes to help us begin to predict future outcomes.

Source: Predicting outcomes with Pattern Recognition: Machine Learning for Algorithmic Trading p. 8

Tutorial page: Predicting outcomes

Hello and welcome to... NO SUBTITLES

Totally dedicated to compare patterns. All the good things are simple: for the pattern of fixed length, we do percentChange() for every nth element and get the abs() of it, so no matter we compare currentPattern vs knownPattern or vice versa. Then, do the avg for all the points similarity and that's it.

Source: Pattern Recognition: Machine Learning for Algorithmic Trading Part 9

Tutorial page: More predicting

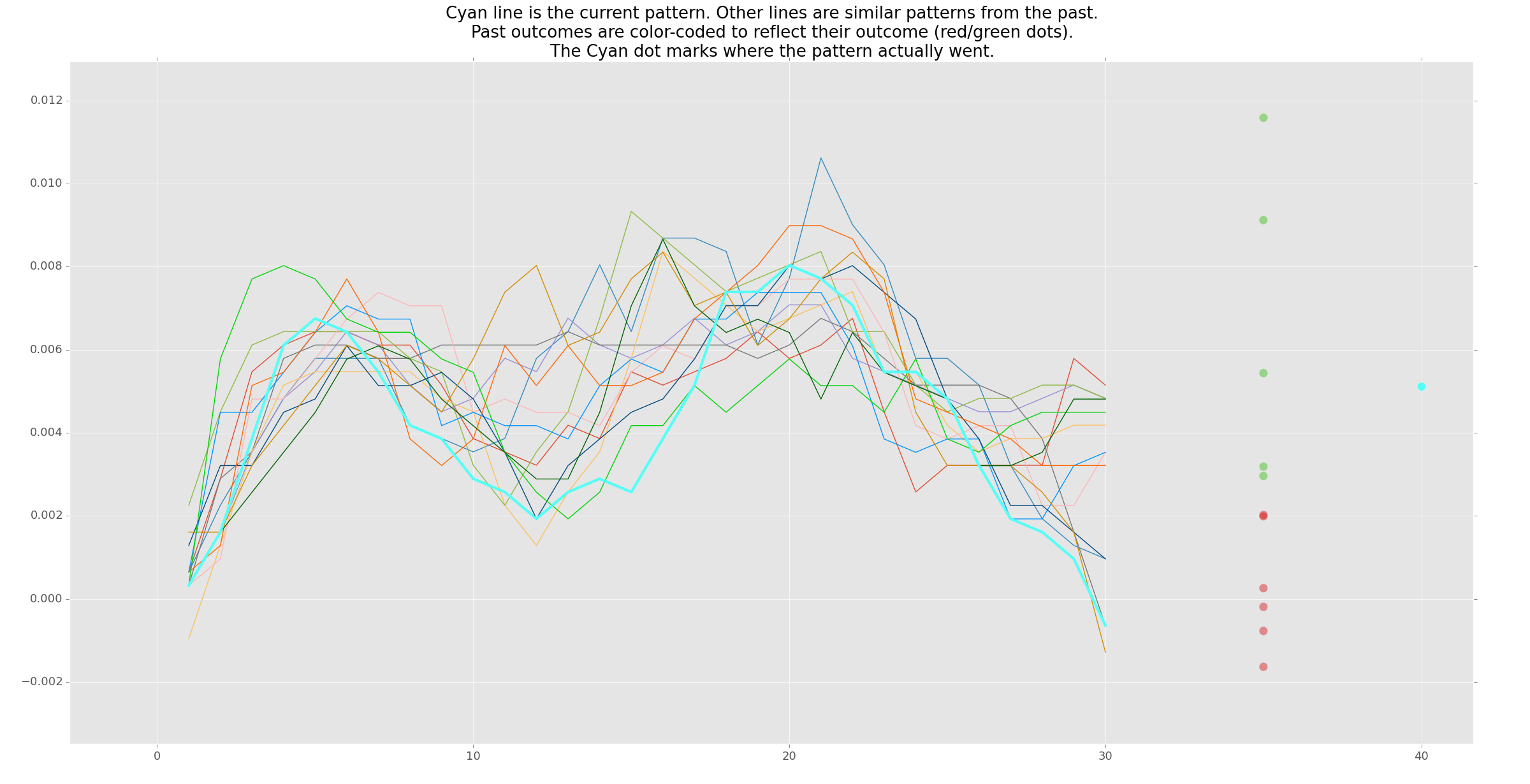

Welcome to the 9th edition of our machine learning course on pattern recognition for algorithmic trading in stocks and Forex. Upon analyzing the most recent pattern, we have determined that its the most likely outcome is a drop. As we look through the patterns we could tell that they were at least somewhat similar just by looking at the numbers. By visually examining the patterns, we can observe that they are somewhat similar, which is evident from the numerical data.

First, obviously, we're going to plot them up with matplotlib here. We have 10 digits basically (pattern consists of 10 points), so x axis or x variable will always be just 1..10: xp = [1,2,3,4,5,6,7,8,9,10] (do it right after we print out the predicted outcome). Next thing we want to have is a figure and so we'll just say: fig=plt.figure(). This is just kind of makes up a figure for matplotlib to plot upon. Next, plot the pattern given for recognition: plt.plot(xp, patForRec). Next, plot the matched pattern: plt.plot(xp, eachPattern). That's it for plotting basically, the only thing we need to do is bring it up with plt.show(). Save that and run this.

We can see very similar lines, close the chart out, this it brings up another chart and this will bring up to the point I mentioned earlier how the beginning is more likely to be more similar than the end. On the chart we can see the result of these lines is slightly different. This line could in theory come back up and further match this but it hasn't more just comparing this pattern. So anyways that one wasn't too sexy, but the next one chart show patterns very close, especially on the end. And continue keeping track of your outcomes and patterns. Now you can display them visually. There's none matched pattertns with above or equal 80% similarity, we can see where the threshold was somewhere between 70 and 80.

So that's going to conclude the ninth video. In the next and tenth video what we're going to be doing is actually lengthening this pattern. Obviously really like the ten plots is just a bit too short for a pattern. Obviously it depends on your timeframe, our timeframe is very, very zoomed in it's a high granularity and so it might make sense to look at longer term patterns or at least a bit longer of a pattern. Instead of 10 points to consider let's consider 30 points and do the same thing that we've done and plot that up. Example of one with 30 points: as you can see it's a similar line a lot more variables in the line and then there's an end divergence here which again is fairly likely using the method that we're doing.

As always, thanks for watching, thanks for all the support, the subscriptions and until next!

-

Hi nice videos :) quick Q when you plot the graphs we see the start is more similar than the ends? (you mention divergence etc) I see why your program does it this way. Would it not be better to look up and compare your patterns in reverse ? so the endings (points on right) are the most similar ? I think the last points are more relevant than the older ones (on left) NO!! ? please explain why you do it this way.

-

Question: is the y-axis pips and the x-axis the amount of points we are looking at? also, does the graph show us that once a pattern is found, GBPUSD usually turns down (declines)

- Answer: The x axis is the plot # in the pattern, the y axis marks % change, not pips.

Lecture 10. Increasing Pattern Complexity: Machine Learning for Algorithmic Trading in Forex and Stocks

In this tutorial, we increase the pattern complexity, ie: increase the pattern length for pattern recognition.

Source: Increasing Pattern Complexity: Machine Learning for Algorithmic Trading in Forex and Stocks

Tutorial page: Increasing pattern complexity

Hello and welcome to the 10th machine learning for use of Forex and stock algo trading automated trading or just plain analysis or just learning to do machine learning! We were plotting up our similar patterns on a matplotlib so we can see them visually, and we said that we wanted to extend our pattern lengths that we're going to look for, and we're going to be looking for a bunch of patterns, not just on the end patterns, eventually, we do need to backtest this.

First, change a couple things here in our percentChange() of formula. It's possible to arrive at a zero percent change, then to calculate the percent change from zero to a point will be problematic for us if that occurs, as we not only expand the length of our pattern, but also we're going to run through all of the patterns. The chances of us hitting something like that is actually pretty likely.

Normally we don't really care if the percentageChange() was zero. What we do care is when we do a percentageChange() of a percentageChange() that yielded a zero that's going to be very hurtful to us so we never want to throw with zero percent change we need something. We're just going to return 0.0000000001, basically zero but we can actually work with this number. So let us solve a few of our issues. Obviously this is not a perfect math but that is the best way to handle a negative infinity when the percentage change of a percentage change of zero comes into question.

...fixing patternStorage() to work with 30 points instead of 10 points...

...fixing currentPattern() to work with 30 points instead of 10 points...

...fixing patternRecognition() to work with 30 points instead of 10 points...

Since we've made the pattern much longer how sim of 70 across one pattern is basically probably not going to happen, very unlikely, that to hit that let's just drop this to 40 just for ease of actually finding a pattern before we start building the backtest, so 40.

Let's go ahead and save this and run and see what the heck we get. Probably you see that our old pattern is right here as well just in case you don't notice.

Conclude this video. In the next video we're going to begin building up our actual backtesting, or running through old data. We were only comparing that most recent plot as being as if the last plot in our data set. However, if we want to back test data, we can do that as well starting at the first plot and then running through each plot as if we were comparing or running through future data. So as we continue getting more plots we're comparing to only the previous plots not the future plots. {maybe plot==point}

So that's what we're going to do in the next videos is actually run through the dataset as if it was reality and start building, saving up that each new pattern it finds, and seeing how long it takes to do this (and you'll see that initially it's very quick), and as we continue getting more and more data and more and more patterns stored the memory, that's when we start actually being taxed or RAM starts to get taxed as that array grows. But anyway, that's what we're gonna start doing the next video is beginning to build the back tester. And really it's quite call it backtester, we're testing against old data, but it's actually better than a backtester. It's really like backtesting the forward test or something I don't know. Anyway that's what we're going to be doing in the next video.

As always, thanks for watching, thanks for the support, for the subscriptions and until next time!

-

Question: Hi and thanks for the tutorial series, great work! Based on the code I've seen so far I assume this would be the correct way to define x and outcome_range: #assume pattern_size to be 10 or 30 min_peek = 20 x = len(avg_line) - (min_peek + pattern_size) outcome_range = avg_line[y + min_peek:y + min_peek + pattern_size] Would this be correct?

-

Question: I'd like to point out that since you are not changing the outcome range, the value of x should remain the same. So, it should still be "x = len(avgLine)-30".

-

Question: Hmmmm i dunno about returning that percentChange as

0.000000001. I think It would be more accurate to just change the startPoint to the closest to 0 value before dividing by it, i'm trying sth like this: stPoint = startPoint if startPoint != 0 else 0.00000000000000000001. Cause with this percentChange formula of ours, the currentPoint can be 0, and it would yield more accurate results, if it would stay 0. What you guyz think? -

Question Hmmm and i think the simularity is not done entirely correctly. If we think about it conceptually 100% - would mean that the numbers are completely the same, where 0% would mean that the numbers are completely different. Now doing 100.00 - {the percentChange} is inaccurate similarity check, cause the percentChange might be more than 100% so then the similarity would be a minus, which conceptually means wat? Its SUPER different? :D . I think the more proper way would be: instead of substracting just from a hundred we should substract from the percentChange of the lowest point and the highest point(in the patternArray , and maybe in the patternArray and the current array?), cause conceptually in the array those would be the actually completely different values. And then in the if 'howSim > ' we would not be checking by a constant number, but by the actual percentage of the completely different value percentChange(the min max points percentChange) like

howSim > minMaxPercChange*0.7. Wat you guyz think? -

Question yikes! p19,p20,p21,p22..... you do a lot with sliding windows over sequences so far...perhaps having a static "window_size" var somewhere and relying on something like:

def window(seq, n=2): """Returns a sliding window (of width n) over data from the iterable. s -> (s0,s1,...s[n-1]), (s1,s2,...,sn), ... """ it = iter(seq) result = tuple(islice(it, n)) if len(result) == n: yield result for elem in it: result = result[1:] + (elem,) yield resultto yield sliding windows of the iterable. then building/storing/analyzing/comparing your patterns with something like:

for i, (w, avg) in enumerate(zip(window(self.avg_line, n=self.window_size), self.avg_line)): # XXXEither way, awesome series! I'm having a lot of fun going through it.

Lecture 11. Pattern Recognition and Outcome: Machine Learning for Algorithmic Trading in Forex and Stocks

Here, we are beginning to compile the past historical patterns that we are comparing to, and taking their eventual outcome for use in future predictions.

Source: Pattern Recognition and Outcome: Machine Learning for Algorithmic Trading in Forex and Stocks

Tutorial page: More on Patterns

Hello and welcome to the 11th machine learning pattern recognition for use with algorithmic automatic trading and with Stocks and Forex! We were just basically looking at the most recent pattern in our data and looking at all the previous patterns in the data and showing the similarity and predicting the outcome. Now that we've done this right, clearly at least visually looking at our pattern recognition, it works pretty well, I mean it's not the best but it works. So we know the pattern recognition works, so we're done. Now we want to know or at least begin to figure out does this even matter. Now we need to go back in time and act as if we were running this in reality. The way that we're going to do this and really recognize new patterns and then see if that actually works.

...cut global patern variables and go down of the script and paste them here...

Basically we want to run through this data as if it was new data so we don't want to load all of the data at the same time. Each time we want to add one plot to the data and then run through and be like: "ok did we know any similar patterns to this current most recent quote-unquote pattern" and go from there. We do this with while loop. Then couple of things that we need to do: dataLength = int(bid.shape[0]) - we need to know where should

the while loop stop. The way we can do this is with bid.shape[0] (so don't forget bid is just part of this numpy array that's defined earlier), because you can not do len(numpy_array). It returns a finicky funky number and convert it back to integer.

Next, where do we want to start. First of all if you started at point number one, there would be no previous data and no way to make a pattern on that data. So since we start at 30 really we must start at 30, but we're probably not going to find it well, we won't find any similar parents because won't have anything to consider. So say toWhat = 100: to what point from the begining we are going to consider.

we'll make a while loop here: while toWhat < dataLength: and basically run the whole program in loop. Create empty arrays inside loop: patternAr = [], performanceAr = [], patForRec = []. Obviously it makes them empty right now but then it starts storing the patterns. Each time we add one data point it clears the patterns and redoes them with patternStorage(); currentPattern(), patternRecogntion().

Efficiency wise bad idea that's going to be very hard on our processing, especially as data length gets longer. You can work around that. That can be fixed very easily. But for the simplicity, and also I don't mean to spoofing everybody this epic machine learning application, either. I'm just trying to teach you machine learning. I'm just pointing that out as well that is going to be a problem area as you start to expand and learn more patterns, but it doesn't have to be a problem, so keep that in mind.

Add toWhat += 1 to make loop not to run infinitely. If it finds any similarities (we have howSim>=40), if anything is found it will plot it up.

Next, make this application stoppable otherwise it will never stop and just continue running through: moveOn = input('press ENTER to continue...'). Save that and let's run.

Just literally hit and hold enter until we find a pattern. It might take a little bit to find its first pattern. Found a pattern similar plots it up for us. Close out of this hit enter again wait till we find another pattern. Sometimes (especially as you get deeper) obviously a very similar pattern plus one point is going to be fairly similar, so once you find a similar one, chances to find a bunch of them.

Now that brings up a point is it brought up a bunch of similar patterns for that exact one pattern. Why we plot them on a different chart? Makes kind of nonsense, so in the next video we show, how to plot them all up on the exact same graph so we can view it all, all the same charts visually.

That way as we build this backtesting we can see visually how it is, and then we can take it one step further, and plot that. Don't forget we have a predicted outcome a percent change so we can plot that percent change. As you can see like here, I found it pretty good positive outcome for that pattern. So with this pattern that we found the predicted outcome is positive. We literally plot those predicted outcomes as well. Since we do know what the future outcome was both on those patterns and also in reality, we can plot that and then we can find out. We can go to the next bit of data and not really the next range of data and we can find out: were we wrong or were we right.

So that's what we're going to continue working towards and getting closer and closer to finding out whether or not this is even of any use at all. But no matter. What you've actually learned is pattern recognition. As we continue we'll be able to find out how useful this is, and then also we're going to start getting pretty deep into some questions of variables and stuff to look forward to.

As always, thanks for watching thank you for your support, subscriptions and until next time!

From YouTube comments: this seems more like a pattern fitting method rather then machine learning.

Lecture 12. Displaying all Patterns Recognized: Machine Learning for Algorithmic Trading in Forex and Stocks

In this video, you are shown how to display all of the patterns at the same time, to make comparing visually easier. Plus it makes for pretty pictures...for all you graph and data lovers out there.

Source: Displaying all Patterns Recognized: Machine Learning for Algorithmic Trading in Forex and Stocks

Tutorial page: Displaying all patterns

Hello everybody and welcome to the 12th machine learning and pattern recognition for stocks and forex trading. We were generating a similar pattern on the chart and now what I would like to do is kind of mesh them all together. If it had maybe five similar patterns, we would have to run cycle through five charts. Let's go ahead and display it all on the exact same chart.